Read our full investment commentary here.

“A 10% decline in the market is fairly common–it happens about once a year. Investors who realize this are less likely to sell in a panic, and more likely to remain invested, benefiting from the wealth building power of stocks.” – Christopher Davis

Market Statistics as of 3/31/25

The first quarter of 2025 (Q1-2025) was the worst for several indices (Nasdaq, S&P 500, Russell 1000 Growth) since 2022. Investors became increasingly concerned about AI-related stocks and their valuations, especially after the Chinese company DeepSeek unveiled an AI model that was much cheaper and used less-advanced chips but appeared to be a strong rival to prominent AI companies like Nvidia, Microsoft, and Google. The gains and valuations on these tech names have been enormous and perhaps it was only a matter of time before investors began to question their values. As you may recall, we have been talking about the valuations and concentration of the Mag 7 names for quite some time, and it began to feel like a broken record, but we know from experience that trees don’t grow to the sky.

As you can see from the chart above, gold was the best performing asset in Q1 followed by fixed income investments and value stocks (Russell 1000 Value), a stark contrast from Q4 2024 and most of 2024. Will this trend continue? That will be in the forefront of our minds. The tech heavy Nasdaq and S&P 500 had a rough go, and the Russell 1000 Growth Index was down almost 10% after being down even more during the quarter. Small caps (Russell 2000) have now entered into a bear market (> -20 %) over the last 52 weeks.

Within the S&P 500 market internals, Energy (+9.30%) was the leading sector followed by Health Care (+6.08), Consumer Staples (+4.58%), Utilities (+4.12), Financials (+3.11%), Real Estate (+2.72%) and Materials (+2.30). On the downside, the Consumer Discretionary sector (-13.97%) led the way and was followed by Information Technology (-12.79%), Communication Services (-6.41%) and Industrials (-0.53%).

As we have often emphasized, our primary concern is protecting our clients’ capital while generating strong risk-adjusted returns that ensure peace of mind. We maintain a laser focus on the companies we invest in and are prepared to make necessary adjustments when needed. Our investment team boasts a wealth of experience, having navigated numerous bear markets and corrections. Although each market downturn is unique, they are all driven by fear and greed. We hope our expertise and experience provide you with a sense of security and confidence.

Portfolio Activity in the First Quarter 2025

During the first quarter, our Value strategy exited its position in McCormick (MKC) due to price strength that appeared to be driven by investors seeking defensive stocks. As a result, we believed the stock price was unwarranted based on the company’s fundamentals. Additionally, we added to our Dollar Tree position (also owned in GARP strategy) as it was a very small position and with the recently announced sale of Family Dollar, we feel management will get back to their core business. We feel that DLTR overpaid for Family Dollar ten years ago and were glad to see them divest that troubled unit.

While there were no new purchases or sales in GARP or International strategy, the Investment Team is focused on the businesses we own and will make changes when we determine that a company is either overvalued, trading below our estimates of what it is worth, or our thesis has changed.

During recent conversations with clients, we have talked at length about the market being expensive, especially in certain names. During the first quarter we witnessed a selloff in companies that had recently been outperformers, and a rotation into other companies. Companies like Phillip Morris (+31%), Nestle (+23%), Safran (+21%), Sony (+19%), Roche(+17%) and Berkshire Hathaway (+17%) all had positive price performance during the quarter while the Magnificent Seven, now the “Lag 7”, dropped 15% (as defined by price performance of the Roundhill Mag 7 ETF).

*Not every client account will have these exact holdings. The actual holdings with respect to any particular client account will vary based on a number of factors including but not limited to: (i) the size of the account, (ii) investment restrictions applicable to the account, if any; and (iii) market exigencies at the time of investment.

“Success in investing isn’t about making a lot of money in a short period of time. It’s about earning reasonable returns over very long periods.”

– Bruce Flatt (CEO of Brookfield)

Thoughts from Tiburon

As soon as the quarter ended, Trump held his “Liberation Day” press conference announcing across the board tariffs, and the markets responded. As many of our readers know, markets hate uncertainty. The intraday moves have been massive and the news flow, or tweets, are changing the direction of bonds and stocks in an instant. Now it seems no one is really interested in what happened in the first quarter as everyone’s attention has turned to tariffs. Jamie Dimon, CEO of JP Morgan, said we are in a “wait and see” period. The folks at LVMH mentioned that we are in “unknown territories” when asked about pricing for the upcoming quarter.

The entire team at LOPW views every dollar that we invest as precious capital. We do not take this lightly. While we all agree that we are in uncertain times, we are committed to helping you navigate these times. I encourage everyone to reread the email that was sent out on Monday April 7th titled “Uncertainty is the only certainty there is…” to give you insight into our current thoughts.

Morgan Housel, an author and blog writer we follow, discusses volatility as the price of admission for equity returns. Similar to paying for a ticket to watch a game, or concert, you must be willing to accept the volatile times in order to earn the returns that equities have provided over time. This is not easy. With the machines controlling so much of the daily flows, the volatility is exacerbated, giving us days when the markets move over 4% in one trading day. While we want to use the volatility to our advantage (i.e., buying when things are ugly and selling when they appear over-valued) we also want to practice patience until we get more clarity. There are still many unknowns in the global economy. We might not get the visibility we desire in the second quarter. Earnings season has commenced, and the calls we have listened to are saying the same thing: “Wait and See.” The good news is that we are earning decent returns, holding cash and patiently waiting for the “fat pitch” across the plate.

We also encourage you to revisit your plan, to make sure that your goals and objectives are being met. During times like these, it is paramount to stay the course and not let outside noise force you into financial decisions that could have a long-term impact on your plan.

DISCLOSURES:

This material is not financial advice or an offer to sell any product and is not a recommendation to buy or sell any particular security. Past performance is not indicative of future results. The opinions expressed are those of the Live Oak Private Wealth Management Investment Team. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass.

Live Oak Private Wealth is a subsidiary of Live Oak Bank. Investment advisory services are offered through LOPW, LLC, an Independent Registered Investment Advisor. Registration does not imply a certain level of skill or training. More information about Live Oak Private Wealth, including our advisory services, fees, and objectives, can be found in our ADV Part 2A or 2B of Form ADV, which is available upon request.

This should not be construed as tax advice. You should always consult with your tax professional with regard to specific tax questions and obligations.

Read our full investment commentary and letter to clients by downloading the first quarter 2025 letter.

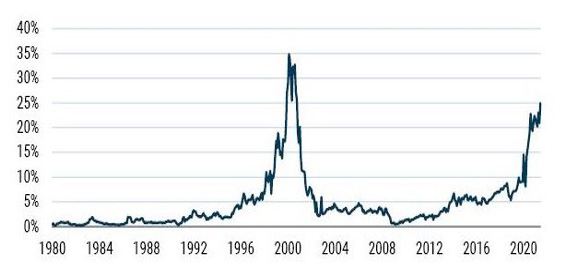

Data from 01/1980 – 06/2021 • Source: GMO, Compustat

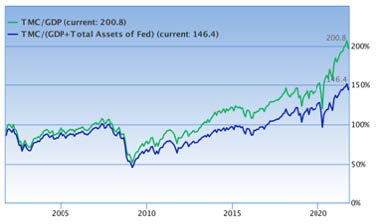

Data from 01/1980 – 06/2021 • Source: GMO, Compustat

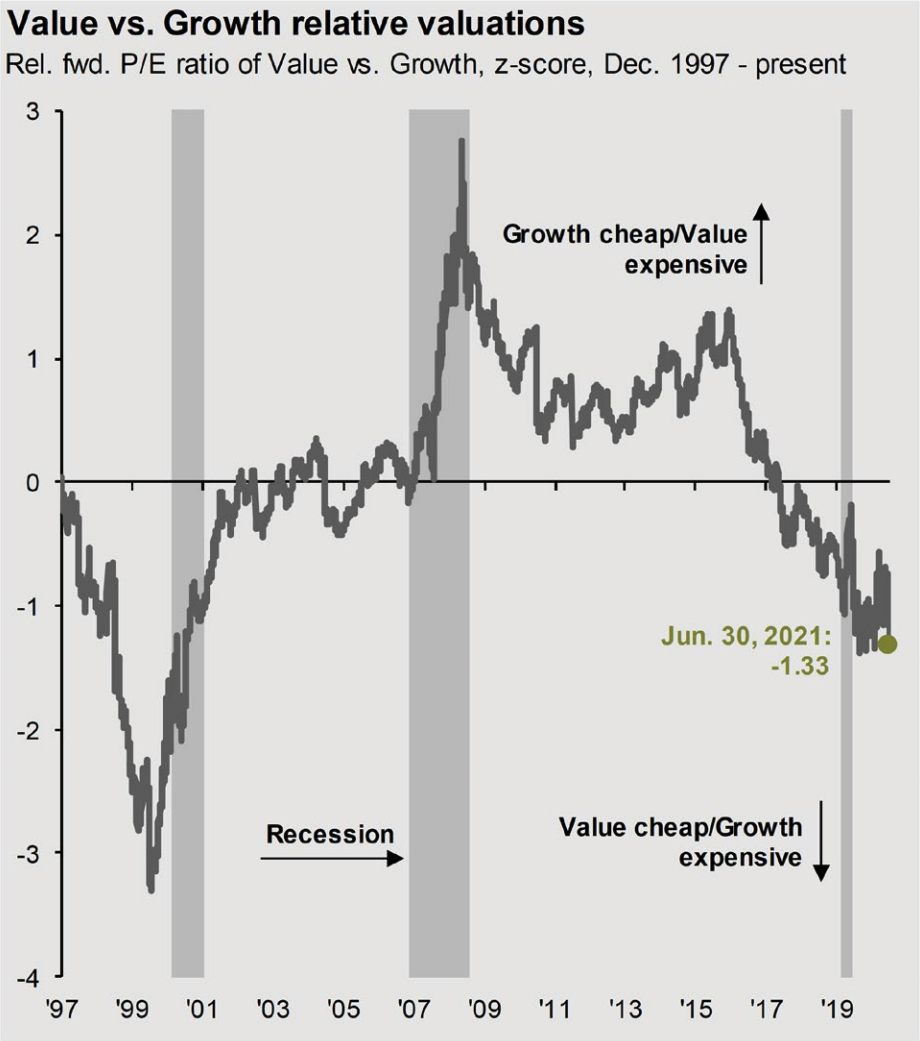

Source: FactSet, FTSE Russell, NBER, J.P. Morgan Asset Management

Source: FactSet, FTSE Russell, NBER, J.P. Morgan Asset Management