Commentary & Thoughts

Last quarter’s letter discussed our framework of investing in growing companies at reasonable prices. We wrote about what we believed to be unreasonable prices being paid for some growth stocks and unproven entities such as SPAC’S and Software (SaaS) stocks. We also referenced some simple valuation math around similar growth stocks from the late 1990s. The tide has seemingly started to recede as the heady valuations of many growth stocks have started coming back to earth since the end of the first quarter. Some of the market darlings of the beginning of the year, such as Tesla, Shopify and the meme stocks have entered correction territory, somewhat related to what is referred to as “re-opening” trades as there has been some rotation to pro-cyclical companies that should benefit from the re-opening of the economy as the vaccines take hold. Covid-winners, like digital transformation and secular growth stocks, have underperformed.

Speaking of the speculative trading frenzy in the meme stocks, such as AMC Entertainment, one has to be taken back by the quote at the beginning of this letter. We can’t recall such a pointed warning in a prospectus before.

As the U.S. economy normalizes further, we expect solid earnings growth from many companies that were negatively affected during the pandemic period. Future earnings growth for these businesses should be quite good, while virus benefactors, Zoom, Peloton and food delivery companies may suffer somewhat.

Long-time readers of our content appreciate our discipline around prices we pay when investing your capital. We have referenced many times that interest rates have trended down from 14% to 0% for the past 40 years. Doubting that they go negative and considering the high probability interest rates normalize to the ranges seen in the early 2000s (4%-10 year Treasury), P/E multiples should contract. We hopefully are positioned in reasonably priced growing businesses where the earnings growth should overcome most of the valuation compression

Second Quarter Portfolio Activity

We again made no changes to our model portfolio. Trading activity was again light and only involved trimming our position in FedEx and adding slightly to AON in a few accounts. The quarter was busy as usual on the research front as we participated in meetings with management from Raytheon and UPS. We also spent time with our friends from long-time investee Brookfield Asset Management learning about a new private equity fund we are interested in. Connor spent the day with the investment team at Markel as they, along with an investment colleague in New York, hosted an informative virtual conference highlighting some new ideas.

Selling is not easy

After a very successful run in FedEx, we opted to trim back the size of our position. Normally, with a good growing business, we don’t like to trim. However, given the circumstances around FedEx’s valuation, as well as the position size in many accounts, we elected (after much handwringing) to trim back the position.

As often said, the hardest decision in investing is deciding when to sell. In the GARP Focused Opportunity strategy, we find selling or trimming difficult. Researching companies, buying, holding, and selling are all tough with all of the dynamics to consider. With selling, there are unique considerations such as the amount of capital gain you incur, opportunity cost and, Charlie Munger’s dogma of never interrupting compounding unnecessarily. We are also reminded of the quote from the great Peter Lynch, “Selling your winners and holding your losers is like cutting the flowers and watering the weeds.”

When we sell or trim, it can create a variety of potential outcomes, such as, the security we sold continues higher while what we allocated your proceeds to declines. Fortunately, we do not feel compelled to immediately reinvest sale proceeds if there is nothing of intelligent value to buy. If we “top tick our sale (trim at what we think might be the highest point in the cycle and the stock declines afterward), we might find ourselves thinking we are smarter than we actually are and could lead us to lose some of the humility needed to be a successful investor.

Trimming position sizes in portfolios can be a prudent exercise in portfolio and risk management, but selling a model position outright (which we haven’t done in quite a while) typically occurs in the event of four possible scenarios:

- Our thesis regarding the investment has changed.

- The valuation (stock price) gets very overvalued relative to business fundamentals.

- Significant management change or poor capital allocation skill is diminishing shareholders’ value.

- We find a company that is superior to the one we are selling.

Our turnover is typically quite low, approximately 20 to 25%. We have positions in companies that we have owned for many years. We do extensive research on a business and the majority of the time, we get the thesis fairly correct. This leads to longterm ownership.

Phil Fisher, the legendary investor and author of “Common Stocks and Uncommon Profits” had a list of 15 points to be considered when evaluating an investment. He was relentless in adherence to these 15 qualities and felt if he checked all boxes, he would rarely need to ever sell. But mistakes of judgment do happen and it is mostly the price paid at the time, but sometimes the thesis. Fisher writes: “When a mistake has been made in the original purchase and it becomes increasingly clear that the factual background of the particular company is, by a significant margin, less favorable than originally believed… then the proper handling of this type of situation is largely a matter of emotional self-control. To some degree, it also depends upon the investor’s ability to be honest with himself.”

In the case with FedEx, we obviously understand the company well and feel like we know the key fundamentals of the delivery business, including UPS. Our first purchase in 2019 proved to be a little early. But who knew a global pandemic would arrive and dramatically alter all stock prices and yet, enhance the delivery business as brick-and-mortar traditional retail moved online and needed to be delivered? We always knew FedEx was a capital-intensive business given the thousands of planes and trucks they operate, not to mention the massive logistical labyrinth the company faces daily. We never liked the capital allocation to the TNT Express acquisition in Europe and watched as FedEx wrote down our shareholder value for more quarters than we would like to admit. What we did do well was buy a lot more shares at a really good price during the virus selloff of last year. That second purchase has proven to be almost a triple, and coupled with our original purchase, a wonderful return. From a risk management perspective, given the position size in many accounts coupled with the valuation, we painstakingly elected to cut the size back to a normal weight.

Hopefully, Peter Lynch would approve. We cut a few flowers and put them in a vase to enjoy while leaving the garden intact

with little weeding needed.

Contributors and Detractors for Focused Opportunity Growth

Our thoughts on positions that had the most positive impact on the strategy for the period ending 6/30/2021

Danaher (DHR) +19.2%

Danaher’s momentum continues with another quarter of strong top-line revenue and bottom-line profit. Strength in its life sciences and medical diagnostics segments were related to tailwinds from COVID-19 effects. The Danaher business system remains focused on accelerating core growth and margin expansion through innovation.

Charter Communications (CHTR) +18.6%

Charter continues to enjoy its strong competitive position as a leader in delivering high-speed broadband and video. Charter’s cable network has significant competitive advantages versus its primary competitors, telephone companies AT&T and Verizon. Free cash flow this past quarter was $1.9B, up from $1.4B a year ago despite higher capital spending.

Moody’s Corporation (MCO) +18.3%

Moody’s is coming off of its biggest quarter ever with revenue of $1.6B. This strength was driven by higher ratings revenue as new bonds came to market in the leveraged loan arena needing to be rated. Moody’s continues to operate very profitably in its cozy duopoly with S&P. Moody’s is one of our more fully valued (expensive) businesses but offers a strong competitive position.

Alphabet, Inc (GOOG) +17.2%

Google had blowout quarterly earnings on the back of its accelerating core search business and rapid growth in YouTube, Google Cloud and Google Play. We remain solidly invested in Google and we are particularly pleased with the efforts and success the company is having by gaining a stronger foothold in the fast-growing public cloud market.

Wells Fargo (WFC) +14.3%

Wells Fargo continues its turnaround and healing from its reputational damage. We remain optimistic about the potential earnings power over the next several years. This next quarter, we expect to see the regulatory-driven asset cap lifted thereby driving much desired and accretive capital reallocation, especially buybacks.

Our thoughts on portfolio positions that had negative or the least positive impact on the strategy for the period ending 6/30/2021

Dollar Tree (DLTR) -14.2%

Dollar Tree Plus (its new format that includes a section with discretionary items that cost more than the traditional $1 Dollar Tree limit) and its combo stores of Family Dollar and Dollar Tree continue to resonate with customers, driving growth. Headwinds, due to shipping and freight costs (due to shortages) have impacted the shares recently. We believe consumer’s desire for convenience and value continues to position the company for future growth.

Walt Disney (DIS) -7.0%

Disney’s impressive content lineup – including Disney, Pixar, Marvel, Star Wars, ABC, ESPN and acquired FOX content – has enabled the company to be a leader in streaming video. Disney management claims to be on track for over 300 million paid streaming subscribers by 2024. By contrast, Netflix has about 208 million today. We remain very comfortable long-term investors in Disney, notwithstanding its premium valuation.

Verizon (VRZ) -3.9%

Verizon remains well positioned as the wireless leader in network quality and reliability. The company’s large loyal customer base is one of its key investment merits. As 5G becomes a reality in the years ahead, we will pay more for that experience and Verizon should profit. Verizon remains more profitable than its competition due to its efficiency and large market share. We remain long-term investors as long as we stay wedded to our phones.

Abbott Labs (ABT) -2.5%

Abbott is taking a breather as much welcomed relief from the vaccines has impacted Abbott’s COVID-19 diagnostic testing machines. Profitability continues to shine in other areas of the company’s business, such as nutritionals and established pharmaceuticals. We like our future growth prospects as Abbott is investing in heart products such as replacement valves. With 60% of sales occurring outside the U.S., we look for long-term growth continuing.

Mastercard (MA) -0.5%

In our opinion, few companies can match Mastercard’s record of consistent, rapid revenue and earnings growth. Mastercard benefits as consumers reemerge from the pandemic and are spending more on credit, debit and prepaid cards. The company continues to adapt to new trends (including threats), such as mobile payments and virtual cards, while pursuing large new opportunities such as business-to-business transactions. Mastercard is another one of our more expensive stocks.

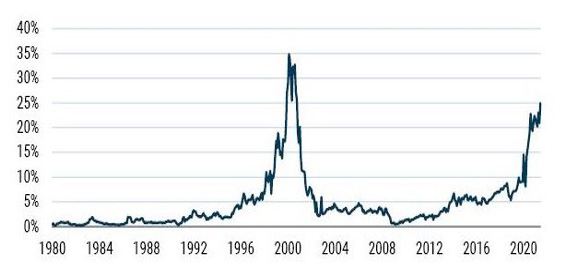

Data from 01/1980 – 06/2021 • Source: GMO, Compustat

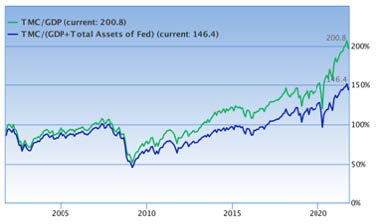

Data from 01/1980 – 06/2021 • Source: GMO, Compustat

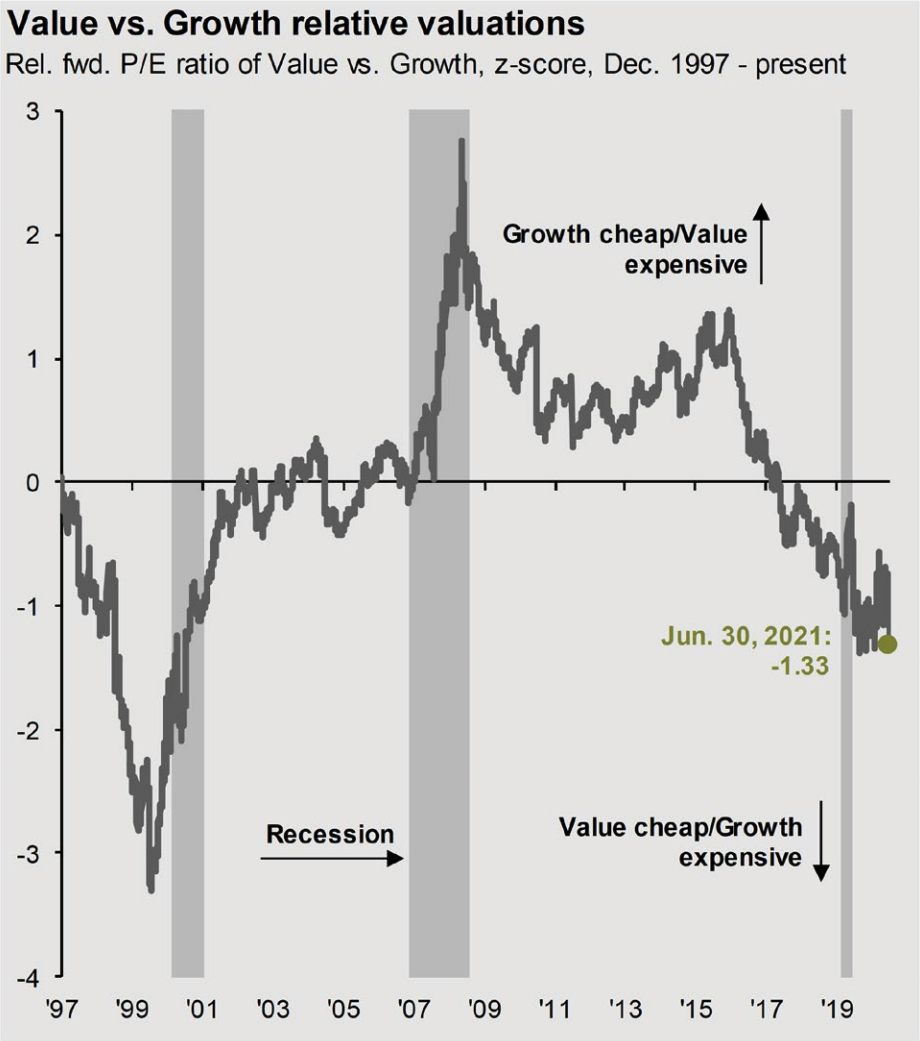

Source: FactSet, FTSE Russell, NBER, J.P. Morgan Asset Management

Source: FactSet, FTSE Russell, NBER, J.P. Morgan Asset Management