Tag Archives: live oak private wealth quarterly letter

Urgency, Emotion, and AI — Fueling Today’s Most Effective Scams. From the LOPW Planning Team.

I hesitated to share this story. After more than 25 years in wealth management – and countless compliance trainings on fraud awareness and prevention – I did not expect to become a victim myself. But I did.

A friend posted a treadmill for sale on social media for $200. I had been wanting to get back into running, and the price was more than reasonable. I messaged her within the app, received payment instructions, and paid. This all happened quickly because the price was too good!

When I followed up and asked about her kids – a topic she normally enjoys – her reply was oddly vague. I texted her directly. Her account had been hacked. The listing was fake. I had sent money to a criminal.

It was only $200. But the lesson was far more valuable: if someone trained to detect fraud can be caught off guard, anyone can.

A New Era of Sophisticated Fraud

Technology has made life more convenient – and given criminals extraordinary tools. Today’s scams are not sloppy emails riddled with typos; they are polished, personalized, and increasingly AIdriven. Criminals use social media to gather personal details and now use generative AI to mimic voices, craft convincing messages, fabricate images, and create deepfake videos with unsettling accuracy.

Their goals remain consistent: bypass logic, exploit emotion, and create urgency.

How Modern Scams Slip Into Daily Life

Understanding how scams unfold helps us recognize red flags sooner. These real-world cases demonstrate how seamlessly advanced scams can become part of daily routines.

When “Normal” Looks Legitimate

A couple selling their second home received what seemed to be a routine email from their title company with updated wiring instructions. The branding looked right, the timing matched their transaction, and nothing appeared suspicious. They wired $480,000 – only to learn criminals had compromised their email weeks earlier and inserted fraudulent instructions at the perfect moment. By the time they discovered the error, the funds were gone.

Modern fraud rarely looks dramatic. It looks routine.

When Impersonation Exploits Trust

Criminals pose as executives, coworkers, vendors, or family members, offering believable reasons why the real person “can’t be reached”. Their goal is simple: sound credible just long enough to pressure someone into acting without verification. These schemes rely on false authority and urgency, which is why all moneymovement instructions should be verified using a known, trusted number – not the one in the message.

Perceived authority alone should never justify bypassing safeguards.

When “Exclusive” Investments Aren’t What They Seem

Affluent investors are frequent targets for “private deals”—preIPO shares, crypto platforms, offshore strategies, or private credit funds. The materials look professional. The referral might even come through someone you trust.

History offers cautionary examples. Bernie Madoff deceived experienced investors and institutions for years. More recently, Sam Bankman-Fried attracted sophisticated venture firms before the collapse of FTX.

Watch for classic signs: consistent returns, pressure to act quickly, vague strategies, internal custody of assets, or resistance to outside review.

Exclusivity can feel flattering. Urgency can feel exciting. Both should prompt caution.

When It Feels Personal

Romance scams often begin with emotion rather than finance. By the time money enters the conversation, trust is already established. Requests for secrecy or movement of funds outside normal advisory channels should end the conversation immediately.

The “family emergency scam” has also surged, powered by public data and AI voice cloning. I recently received a call from a nearby town – where my teenage daughter happened to be that evening. A panicked voice cried, “Mom… come get me…” followed by a man telling me she had been in an accident and asking me to confirm her name and age. That request was the red flag. In a real emergency, they should supply identifying information – not ask for it. I hung up and called my daughter. She was safe.

These schemes work because fear triggers action before logic.

Criminals count on panic to override process.

When Older Adults Are Targeted

Older adults are increasingly targeted with impersonation, investment, romance, and “grandparent” scams, with many cases exceeding six figures. Common tactics include fake IRS, Social Security, or Medicare calls, tech support popups seeking remote access or payment, lotteryfee scams, and utilityshutoff threats demanding immediate payment.

These schemes exploit trust, isolation, and fear.

Why Fraud Works – And How to Protect Yourself

Fraud is less about knowledge and more about timing. It succeeds when people are distracted, stressed, rushed, grieving, or reacting emotionally. Urgency and impersonation shortcircuit rational thinking.

Victims are not foolish – they are human.

The strongest defense against fraud is discipline – simple, repeatable habits that protect you when emotion runs high. Discipline involves recognizing warning signs and adopting core practices.

Recognize the Warning Signs

Unexpected contact requesting money or sensitive information

Instructions to send cryptocurrency, buy gift cards, or use payment apps for “secure” transfers

Pressure to act immediately or keep the request secret

Appeals to strong emotion – fear, excitement, panic, love

Adopt These Core Practices

Never share account numbers, passwords, Social Security numbers, or verification codes

Independently verify wiring instructions using a known phone number

Be skeptical of “toogoodtobetrue” opportunities and avoid pressure to move quickly

Don’t click unfamiliar links or scan unknown QR codes – type the URL yourself

Slow down on purpose; a 10minute pause is often enough to expose a lie

Loop in your advisor – a second set of eyes restores process and neutralizes urgency

Four Important Questions to Ask Yourself

Before sharing personal information or transferring funds, pause and ask:

Is this urgent?

Did it arrive unexpectedly?

Is there pressure for secrecy?

Am I being asked to bypass a normal process?

If even one answer is yes – stop. Call a trusted contact. Verify independently. Take a breath.

Fraud depends on speed; slowing down breaks its rhythm.

Final Thoughts

Scams will continue to evolve. AI will make them more convincing, and social media will make them more personal. Yet the criminal’s objective remains the same: create enough urgency, authority, or emotional pressure to override normal caution.

The solution is equally consistent: pause, verify, and follow established processes.

Even experienced professionals can be caught off guard. What protects us is not confidence – it is discipline. And sometimes, it is simply hanging up the phone.

Safeguarding our clients’ assets remains central to our fiduciary responsibility. If something doesn’t feel right – call your advisor first.

DISCLOSURES:

This material is not financial advice or an offer to sell any product and is not a recommendation to buy or sell any particular security. Past performance is not indicative of future results. The opinions expressed are those of the Live Oak Private Wealth Management Investment Team. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass.

Live Oak Private Wealth is a subsidiary of Live Oak Bank. Investment advisory services are offered through LOPW, LLC, an Independent Registered Investment Advisor. Registration does not imply a certain level of skill or training. More information about Live Oak Private Wealth, including our advisory services, fees, and objectives, can be found in our ADV Part 2A and/or Form CRS, which is available upon request.

This should not be construed as tax advice. You should always consult with your tax professional with regard to specific tax questions and obligations.

Read our full investment commentary here.

“A 10% decline in the market is fairly common—it happens about once a year. Investors who realize this are less likely to sell in a panic, and more likely to remain invested, benefitting from the wealth building power of stocks” – Christopher Davis

Market Statistics as of 3/31/26

The first quarter of 2026 (Q1 2026) was a tale of two markets for many of the indices and very reminiscent of Q1 2025 where value stocks outperformed growth stocks and bonds. The markets were trending higher for most of the first quarter until the air strikes began on February 28 and the resulting peak to trough S&P 500 decline of 9.1% pushed the markets close to the 10% decline that Wall Street characterizes as a correction. We actually hit that level in early April but have regained much of those losses since then. We have said in many quarterly letters and calls over the years that these markets can move extremely quickly and violently in both directions depending upon headlines and how the algorithms interpret the data. We know that these minute to minute and day to day gyrations are usually not indicative of the true value of the underlying businesses we invest in. Therefore, we try to tune out much of the “noise” and look out for where we believe the earnings will be trending in the future. Earnings season is quickly approaching, and we will be listening to how the current situation in the Middle East is affecting our companies.

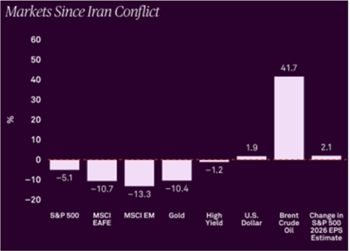

As you can see from the chart above, gold was the best performing asset in Q1 (just like Q1 2025) followed by mid caps (S&P Mid Cap) and value stocks (Russell 1000 Value). Within the S&P 500 market internals, energy led the way and was the only sector to post gains in March, (10.40%) and (38.20%) in Q1, its best quarter since Q1 ’22. Whether energy prices are higher for longer or based on the war is a major issue. Many oil pundits claim there is a worldwide glut of oil, but rig counts and global drilling suggest something different. Like we say, it takes two sides to make a market, and we are paying close attention to the matter. Materials (9.30%) was the next best sector followed by utilities (7.52%), consumer staples (7.01%), industrials (4.30%) and real estate (1.94%). On the downside, the financials sector (-9.80%) led the way and was followed by consumer discretionary (-9.34%), information technology (-9.25%), communication services (-7.10%) and health care (-5.29%).

Thoughts from Tiburon

“There is an excitable dog on a very long leash, darting randomly in every direction. At any moment, there is no predicting which way the pooch will lurch. He leaps randomly from one direction to the next, stops to smell every leaf, barks at other dogs. And jumps behind you for no reason. His movements are totally unpredictable.

But in the long run, you know he is heading northeast at an average speed of three miles per hour, because that’s where the owner is taking him. What is astonishing is that almost all of the market players, big and small, seem to have their eye on the dog, and not the owner.” – Ralph Wagner

EPS=earnings per share. EM=emerging markets. Returns from 02.27.26 close to 03.31.2026 close. MSCI index returns in USD. Sources: Bloomberg L.P.; FactSet; BNY.

In February, the conflict with Iran increased market volatility. The analogy of Mr. Wagner’s quote is important to note during times of increased VIX. Said another way, stock price does not equal business valuation. Stock price reflects the valuation plus or minus current sentiment, which can create opportunities for investors. As reflected in the chart above, most asset classes declined following the onset of the conflict, with the exception of oil and the U.S. dollar. A key risk we continue to monitor is the potential impact on overall economic growth, particularly as higher gas prices affect broad segments of the economy. An important concern is whether higher interest rates will prove persistent. While expectations entering 2026 included approximately 50 basis points of rate cuts, current market pricing reflects no cuts, with some projections now pointing to potential rate increases. While moderate rate increases are manageable, returns tend to suffer if rates rise too fast or too high.

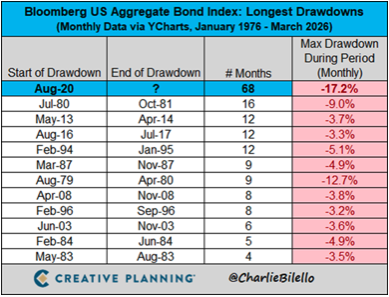

Market strategist Charlie Biello recently noted the US bond market has now been in a drawdown for 68 months, by far the longest in history, as illustrated in the chart below. This has resulted in additional losses for investors trying to stretch their maturities out further to increase their yields. Rest assured, we have taken and continue to take a very conservative approach to our fixed income investments with investment grade quality and short-term maturities being our strategy. We view our fixed income money as a safe haven, not meant for aggressive capital appreciation and undue risk.

For most of the past decade, the group of tech stocks called the Magnificent 7 (“MAG 7” ) have outperformed. The strength in this group made the term a household name. Recently, a new theme has emerged called HALO (Heavy Assets, Low Obsolescence). Highlighted by Goldman Sachs Research, the strategy targets businesses with significant physical assets that are difficult to replicate due to high costs, regulation, long build times, or engineering complexity, and that retain long‑term economic relevance. Examples include utilities, grids, pipelines, transportation infrastructure, critical machinery, and long‑cycle industrial capacity.

The valuation gap between capital‑intensive and capital‑light businesses has narrowed meaningfully. Although fund flows increasingly favor HALO assets, positioning remains relatively light as investors diversify away from crowded technology names. While rotation toward these sectors appears underway, long‑term allocations are still modest.

Technology remains overweight by historical standards, while sectors such as energy, utilities, and materials are underrepresented. Even a modest reallocation could drive significant upside, though the durability of this strategy in algorithm‑driven markets remains uncertain.

As we have said in many (maybe all) of these quarterly newsletters, our primary concern is protecting our clients’ capital while generating strong risk-adjusted returns that ensure peace of mind. We are constantly focused on the companies we invest in and are prepared to make the necessary adjustments when needed. Our investment team boasts a wealth of experience, having navigated numerous corrections and bear markets. Each market downturn is unique and usually the result of something not obvious, but they all are driven by fear and greed. We hope our experience and knowledge provide you with a sense of security and confidence. As always, thank you for your trust in us.

Portfolio Activity in the First Quarter 2026

Portfolio activity for the Value strategy was light with some trimming and adding to existing positions where our weightings were over or under our desired target sizes. We did exit a very small position in Solstice (SOLS), which was a recent spinoff from Honeywell (HON) and one we did not want to add to our Value strategy.

We added Lennar (LEN) to our Garp Model in January. LEN is the 2nd largest homebuilder in the US. LEN transitioned from a traditional builder into a capital light version by offloading long-term land development risks to third-party partners (like Millrose Properties). This “asset light” model allows them to control land with less money upfront. This should free up cash flow and in turn produce higher ROIC. We believe the current housing shortage will provide a long-term tailwind for this company.

Additionally, we trimmed our position in Alphabet (GOOG) in January. Google was and remains one of our top equity positions. The strength in the stock created an outsized position in some accounts. We continued to like the business, just thought it made sense to take some chips off the table.

In the International strategy we added London Stock Exchange (LSEGY). LESGY is a leading global financial infrastructure and data provider, like Bloomberg, S&P Global, and Intercontinental Exchange. With 44,000 customers in 170 countries, the company is integral to providing data and plumbing to the global financial system, utilizing a recurring revenue model. During the recent “SaaSmageddon” selloff, subscription-based software and data providers were broadly and indiscriminately sold. We viewed this dislocation as an attractive opportunity to initiate a position in a business whose earnings power is driven primarily by high-quality, recurring revenues.

DISCLOSURES:

This material is not financial advice or an offer to sell any product and is not a recommendation to buy or sell any particular security. Past performance is not indicative of future results. The opinions expressed are those of the Live Oak Private Wealth Management Investment Team. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass.

Live Oak Private Wealth is a subsidiary of Live Oak Bank. Investment advisory services are offered through LOPW, LLC, an Independent Registered Investment Advisor. Registration does not imply a certain level of skill or training. More information about Live Oak Private Wealth, including our advisory services, fees, and objectives, can be found in our ADV Part 2A and/or Form CRS, which is available upon request.

This should not be construed as tax advice. You should always consult with your tax professional with regard to specific tax questions and obligations.

Get Live Oak Private Wealth’s perspective on the shifting investment patterns and the impact on clients by downloading our 2025 Year-End Letter.

“The key to investing is not assessing how much an industry is going to affect society, or how much it will grow, but rather determining the competitive advantage of any given company and, above all, the durability of that advantage.” – Warren Buffett | July 1999

Get Live Oak Private Wealth’s perspective on the shifting investment patterns and the impact on clients by downloading our 2025 Year-End Letter.

“A 10% decline in the market is fairly common–it happens about once a year. Investors who realize this are less likely to sell in a panic, and more likely to remain invested, benefiting from the wealth building power of stocks.” – Christopher Davis

Market Statistics as of 3/31/25

The first quarter of 2025 (Q1-2025) was the worst for several indices (Nasdaq, S&P 500, Russell 1000 Growth) since 2022. Investors became increasingly concerned about AI-related stocks and their valuations, especially after the Chinese company DeepSeek unveiled an AI model that was much cheaper and used less-advanced chips but appeared to be a strong rival to prominent AI companies like Nvidia, Microsoft, and Google. The gains and valuations on these tech names have been enormous and perhaps it was only a matter of time before investors began to question their values. As you may recall, we have been talking about the valuations and concentration of the Mag 7 names for quite some time, and it began to feel like a broken record, but we know from experience that trees don’t grow to the sky.

As you can see from the chart above, gold was the best performing asset in Q1 followed by fixed income investments and value stocks (Russell 1000 Value), a stark contrast from Q4 2024 and most of 2024. Will this trend continue? That will be in the forefront of our minds. The tech heavy Nasdaq and S&P 500 had a rough go, and the Russell 1000 Growth Index was down almost 10% after being down even more during the quarter. Small caps (Russell 2000) have now entered into a bear market (> -20 %) over the last 52 weeks.

Within the S&P 500 market internals, Energy (+9.30%) was the leading sector followed by Health Care (+6.08), Consumer Staples (+4.58%), Utilities (+4.12), Financials (+3.11%), Real Estate (+2.72%) and Materials (+2.30). On the downside, the Consumer Discretionary sector (-13.97%) led the way and was followed by Information Technology (-12.79%), Communication Services (-6.41%) and Industrials (-0.53%).

As we have often emphasized, our primary concern is protecting our clients’ capital while generating strong risk-adjusted returns that ensure peace of mind. We maintain a laser focus on the companies we invest in and are prepared to make necessary adjustments when needed. Our investment team boasts a wealth of experience, having navigated numerous bear markets and corrections. Although each market downturn is unique, they are all driven by fear and greed. We hope our expertise and experience provide you with a sense of security and confidence.

Portfolio Activity in the First Quarter 2025

During the first quarter, our Value strategy exited its position in McCormick (MKC) due to price strength that appeared to be driven by investors seeking defensive stocks. As a result, we believed the stock price was unwarranted based on the company’s fundamentals. Additionally, we added to our Dollar Tree position (also owned in GARP strategy) as it was a very small position and with the recently announced sale of Family Dollar, we feel management will get back to their core business. We feel that DLTR overpaid for Family Dollar ten years ago and were glad to see them divest that troubled unit.

While there were no new purchases or sales in GARP or International strategy, the Investment Team is focused on the businesses we own and will make changes when we determine that a company is either overvalued, trading below our estimates of what it is worth, or our thesis has changed.

During recent conversations with clients, we have talked at length about the market being expensive, especially in certain names. During the first quarter we witnessed a selloff in companies that had recently been outperformers, and a rotation into other companies. Companies like Phillip Morris (+31%), Nestle (+23%), Safran (+21%), Sony (+19%), Roche(+17%) and Berkshire Hathaway (+17%) all had positive price performance during the quarter while the Magnificent Seven, now the “Lag 7”, dropped 15% (as defined by price performance of the Roundhill Mag 7 ETF).

*Not every client account will have these exact holdings. The actual holdings with respect to any particular client account will vary based on a number of factors including but not limited to: (i) the size of the account, (ii) investment restrictions applicable to the account, if any; and (iii) market exigencies at the time of investment.

“Success in investing isn’t about making a lot of money in a short period of time. It’s about earning reasonable returns over very long periods.”

– Bruce Flatt (CEO of Brookfield)

Thoughts from Tiburon

As soon as the quarter ended, Trump held his “Liberation Day” press conference announcing across the board tariffs, and the markets responded. As many of our readers know, markets hate uncertainty. The intraday moves have been massive and the news flow, or tweets, are changing the direction of bonds and stocks in an instant. Now it seems no one is really interested in what happened in the first quarter as everyone’s attention has turned to tariffs. Jamie Dimon, CEO of JP Morgan, said we are in a “wait and see” period. The folks at LVMH mentioned that we are in “unknown territories” when asked about pricing for the upcoming quarter.

The entire team at LOPW views every dollar that we invest as precious capital. We do not take this lightly. While we all agree that we are in uncertain times, we are committed to helping you navigate these times. I encourage everyone to reread the email that was sent out on Monday April 7th titled “Uncertainty is the only certainty there is…” to give you insight into our current thoughts.

Morgan Housel, an author and blog writer we follow, discusses volatility as the price of admission for equity returns. Similar to paying for a ticket to watch a game, or concert, you must be willing to accept the volatile times in order to earn the returns that equities have provided over time. This is not easy. With the machines controlling so much of the daily flows, the volatility is exacerbated, giving us days when the markets move over 4% in one trading day. While we want to use the volatility to our advantage (i.e., buying when things are ugly and selling when they appear over-valued) we also want to practice patience until we get more clarity. There are still many unknowns in the global economy. We might not get the visibility we desire in the second quarter. Earnings season has commenced, and the calls we have listened to are saying the same thing: “Wait and See.” The good news is that we are earning decent returns, holding cash and patiently waiting for the “fat pitch” across the plate.

We also encourage you to revisit your plan, to make sure that your goals and objectives are being met. During times like these, it is paramount to stay the course and not let outside noise force you into financial decisions that could have a long-term impact on your plan.

DISCLOSURES: This material is not financial advice or an offer to sell any product and is not a recommendation to buy or sell any particular security. Past performance is not indicative of future results. The opinions expressed are those of the Live Oak Private Wealth Management Investment Team. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass.

Live Oak Private Wealth is a subsidiary of Live Oak Bank. Investment advisory services are offered through LOPW, LLC, an Independent Registered Investment Advisor. Registration does not imply a certain level of skill or training. More information about Live Oak Private Wealth, including our advisory services, fees, and objectives, can be found in our ADV Part 2A or 2B of Form ADV, which is available upon request.

This should not be construed as tax advice. You should always consult with your tax professional with regard to specific tax questions and obligations.

Read our full investment commentary and letter to clients by downloading the first quarter 2025 letter.

The Role of Trusts in Estate Planning:

Insights from the Philip Seymour Hoffman Estate

When the Oscar-winning actor Philip Seymour Hoffman’s life and career abruptly ended in 2014 after passing away from a drug overdose at the age of 46, he left his heirs with a sizable estate valued at $34 million. Hoffman was survived by three children and a long-time partner, Mimi O’Donnell, who was also the mother of his children. Before Hoffman’s death, it was reported that he expressed a desire for his children to develop a strong work ethic and to avoid the potential pitfalls associated with being “trust fund kids.” Consequently, he bequeathed his entire estate outright to Ms. O’Donnell.

The phrase “trust fund kid” is prevalent in our popular culture, frequently carrying a negative connotation that individuals who benefit from trusts are excessively privileged and may not have to engage in work for their livelihood. In addition, the world of trusts in estate planning can seem complicated and complex and are often portrayed as vehicles that only benefit affluent families. However, trusts serve multiple significant and positive functions in estate planning, many of which contradict common misconceptions in cultural views about trusts.

Common Trust Objectives

For many individuals, a will-only based estate plan may be sufficient to accomplish their goals regarding the distribution of their estate to their designated beneficiaries. However, trusts allow for additional protections and strategies that a will-only based plan cannot offer.

By establishing a trust, the trust creator, also known as the grantor, can achieve a range of objectives. The most common include:

providing support for family in the event of incapacity, illness, or disability

avoiding the state-specific probate process and providing privacy for beneficiaries

reducing a taxable estate, thereby minimizing estate taxes

protecting assets from creditors and from divorce

establishing a legacy and supporting a valued charity

The various objectives and purposes of different types of trusts are crucial to understand for anyone considering their estate planning options. There are numerous types of trusts, each designed to fulfill specific needs and goals, such as revocable living trusts, irrevocable trusts, charitable trusts, and special needs trusts, among others. Each type of trust has its unique characteristics, benefits, and limitations, which can significantly influence an individual’s decision-making process regarding their estate plan.

Types of Trusts: Revocable vs. Irrevocable Trusts

Trusts can be classified as either revocable or irrevocable. A revocable trust permits the grantor to alter the trust terms during their lifetime while competent, whereas an irrevocable trust does not allow for any changes to the trust terms unless approved by the court or the beneficiaries of the trust.

The grantor’s purpose and objectives for establishing a trust determines whether a revocable or irrevocable trust is created. The modifiable nature of revocable trusts provides greater flexibility compared to irrevocable trusts, making them a popular planning option. However, assets held by a revocable trust are included in the grantor’s taxable estate and are subject to estate taxes upon the grantor’s death. Additionally, revocable trusts do not offer protection against creditor claims and lawsuits involving the grantor. On the other hand, irrevocable trusts cannot be altered once established; however, they can remove assets from the grantor’s taxable estate and provide asset protection benefits.

Revocable and irrevocable trusts funded during the grantor’s lifetime both provide privacy and avoid probate.

Types of Trusts: Testamentary vs. Living Trusts

Testamentary trusts are established upon the grantor’s death. A testamentary trust is created within the terms of the grantor’s last will and testament and remains inactive and unfunded until the grantor’s death. A grantor can amend their will during lifetime, but after death, any trust created within the will is irrevocable and cannot be changed.

In contrast, a living trust, also referred to as an inter vivos trust, is established before a grantor’s death and is administered by a trustee during and after the grantor’s life. Consequently, living trusts offer the grantor greater control over the management and execution of the trust compared to testamentary trusts, which are established upon the grantor’s death. Living trusts can be revocable or irrevocable.

Benefits of Utilizing Trusts

Returning to Philip Seymour Hoffman, what benefits could his estate have recognized if he had included trusts for his heirs in his estate plan?

Flexibility to Address the Decedent’s Wishes. Trusts can be tailored with specific provisions surrounding when and how heirs inherit assets, addressing concerns like those of Hoffman about “trust fund kids.” For example, a trust might require beneficiaries to earn their own income before receiving distributions, promoting a work ethic and financial independence.

Probate Avoidance or Minimization. Since assets held in trust typically avoid the probate process, it is likely that the Hoffman estate could have avoided the complexities and potential pitfalls associated with probate had he incorporated a revocable trust agreement into his estate plan.

Holding assets in trust offers more privacy for families, as trust assets typically remain out of public record, unlike those in probate. After Hoffman’s will was filed, The New York Post published it, exposing his wishes to the public. Unlike celebrities, most individuals face less scrutiny, but probate allows anyone to access details about a deceased person’s assets and beneficiaries, potentially leading to unwanted attention or exploitation.

The probate process can take months or years to complete. Assets held in trust can continue to be managed without interruption should the grantor or beneficiary die or become disabled. Upon death or disability of the grantor or a beneficiary, the designated trustee would continue to manage the property for the benefit of the successive beneficiaries. According to the New York County Surrogate’s Court online database, the Hoffman estate is not yet closed as of this writing, 11 years later.

The probate process can be expensive due to court costs and legal fees. In North Carolina, the Clerk of Court currently charges probate fees equal to 0.4% (or $4/$1,000) of the value of the estate’s probate property (up to a maximum of $6,000).

Tax Planning and Efficiency. Hoffman’s estate tax liability, which was approximately $15 million, could have been reduced had assets been placed in trust since the gift to his partner did not qualify for the marital deduction. The U.S. federal tax code allows for the transfer of assets between spouses without incurring estate tax at the first spouse’s death, effectively deferring the tax liability until the surviving spouse’s death. However, in Hoffman’s case, since the recipient of the gift was not a spouse, the transfer would not have met the criteria for the marital deduction.

Estate Planning Lock. The final allocation of Hoffman’s wealth to his children will be decided by their mother’s estate plan. What does this look like if their mother does not have a will? What if she marries and/or has additional children before her passing? Hoffman clearly believed that the mother of his children would provide for them appropriately; however, trusts offer the flexibility to incorporate these planning decisions into one’s own plan so that the plan is locked in at the initial wealth transfer. Following the death of a spouse or partner, life can evolve. Oftentimes when second families are involved, estate planning can become more intricate and nuanced. Trusts can be helpful tools for navigating those intricacies.

Reports indicate that Hoffman’s accountant and attorney recommended he designate assets for his children in his estate plan. The reasons behind Hoffman’s decision to disregard his advisors’ counsel will remain unclear; he was brilliant in his own right and may have wished to avoid the “tax tail from wagging the dog”, or simply wanted to uphold his desire that his children would not be overly reliant on inherited wealth while showing his trust in their mother to manage the estate responsibly and in a manner that would benefit their family as a whole. However, other estate planning objectives such as incapacity planning, privacy, probate avoidance, tax minimization, asset protection, and charitable goals are important for many. Incorporating a trust as part of your estate plan can help achieve these objectives and provide assurance that your assets will continue to benefit future generations. Trusts can be established in numerous ways, with virtually countless variations available; therefore, the guidance of a qualified estate planning attorney is highly recommended.

Live Oak Private Wealth offers trust and estate planning strategy discussions as an integral component of our comprehensive financial planning services. Should you have any inquiries regarding how various trusts may benefit your family, we would be pleased to discuss this with you.

DISCLOSURES: This material is not financial advice or an offer to sell any product and is not a recommendation to buy or sell any particular security. Past performance is not indicative of future results. The opinions expressed are those of the Live Oak Private Wealth Management Investment Team. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass.

Live Oak Private Wealth is a subsidiary of Live Oak Bank. Investment advisory services are offered through LOPW, LLC, an Independent Registered Investment Advisor. Registration does not imply a certain level of skill or training. More information about Live Oak Private Wealth, including our advisory services, fees, and objectives, can be found in our ADV Part 2A or 2B of Form ADV, which is available upon request.

This should not be construed as tax advice. You should always consult with your tax professional with regard to specific tax questions and obligations.

Read our full investment commentary and letter to clients by downloading the first quarter 2025 letter.

Get Live Oak Private Wealth’s perspective on the shifting investment patterns and the impact on clients by downloading our 2024 Year-End Letter.

“It shouldn’t come as a surprise that the return on investment is significantly a function of the price paid for it. For that reason, investors clearly shouldn’t be indifferent to today’s market valuations.” – Howard Marks

Get Live Oak Private Wealth’s perspective on the shifting investment patterns and the impact on clients by downloading our 2024 Year-End Letter.

Read our full investment commentary and letter to clients by downloading the Q3 2024 quarterly letter.

“October: This is one of the peculiarly dangerous months to speculate in stocks. The others are July, January, September, April, November, May, March, June, December, August, and February.” -Mark Twain

What a difference a year can make in the capital markets! As we were writing the 2023 Q3 newsletter last year, it felt like chaos was reigning in the stock and bond markets.

Read our full investment commentary and letter to clients by downloading the third quarter 2024 letter.

Read our full investment commentary and letter to clients by downloading the Q1 2024 quarterly letter.

“The desire to perform all the time is usually a barrier to performing over time.” – Robert Olstein

As 2023 drew to a close, speculation around Fed Chairman Jerome Powell’s comments on potential rate cuts fueled a strong rally. The momentum continued into the first quarter of 2024, resulting in gains across all equity indices. However, the attitude towards interest rates now seems to suggest that rates will be higher for longer and how that will influence the market returns remains to be seen in the year ahead.

Read our full investment commentary and letter to clients by downloading the first quarter 2024 letter.

You are about to leave the Live Oak Private Wealth website.

Disclaimer: This link will take you to a website outside of the Live Oak Private Wealth site. The new site may offer a different privacy policy and level of security. Live Oak Private Wealth is not responsible for the products or services that are offered or expressed on other websites.