By: Live Oak Private Wealth

Introduction

“We believe that the recent volatility and our current market price reflect market and trading dynamics unrelated to our underlying business, or macro or industry fundamentals, and we do not know how long these dynamics will last. Under these circumstances, we caution you against investing in our Class A common stock, unless you are prepared to incur the risk of losing all or a substantial portion of your investment.”

– AMC Entertainment prospectus language, May 2021

This quarter, on May 26, the Dow Jones Industrial Average turned 125 years old. The index of 12 industrial companies closed that first day of trading, May 26, 1896 at 40.94. Since that day, the Dow has certainly evolved with the U.S. economy through the Great Depression, two world wars and other events, such as the terrorist attack of 9/11, that have embodied the 20th and early 21st centuries.

The Dow has risen an average of 7.69% per year since 1896 according to historical data from the Wall Street Journal. This is a simple arithmetic average and investors’ actual returns could have been quite different (considering the full range of annual changes over the past 105 years of -52.67% in 1931 to a high of 66.69% in 1933). It first climbed above 100 in 1906, topped 1,000 in 1972 and crossed 10,000 in 1999. When Frank started his investment career in 1981, the Dow was around 933. Bill started in 1986 and the Dow was around 1,700. To think that now the Dow is trading around 34,000 is somewhat remarkable, but is a worthy reminder of the power of compounding and the benefits of staying invested through thick and thin.

Charles Dow, who was the first editor of the Wall Street Journal and Edward Jones, created the industrial, smokestackfocused gauge to help explain stock market movements to the Journal readers. The roster of companies in the Index expanded to 20 from 12 in 1916, and to 30 companies (where it stands today) in 1928. Procter and Gamble, which was added in 1932, is the longest running member of the Index since General Electric departed the Index in 2018. Well-known stocks that have come and gone over the years include Studebaker, Sears, Woolworth, and Kodak. Newcomers now give the Dow more of a “non-industrial flavor” with the likes of Salesforce.com, Amgen and Apple.

The Dow Jones Industrial Average will always remain the bellwether measurement indicator when someone asks, “What did the market do today?” Other pertinent indexes such as the S&P 500 and NASDAQ are quite relevant as important measurements as well. A lot of “how the market did today” is determined by how United Healthcare, Goldman Sachs, Home Depot and Microsoft do because the Dow is a dollar-price weighted index, meaning the higher the constituent’s share price is, the more influence that stock has on the Index that day. Walgreens, Cisco Systems, Coke, and Verizon need large moves in their daily prices to move the index due to their lower share prices relative to the larger firms.

Happy 125th birthday to the Dow Jones Industrial Average!

Market Statistics as of June 30, 2021

| Index | 2021 2nd Qtr | 2021 YTD 6 Months |

|---|---|---|

| DJIA | 5.08% | 13.79% |

| S&P 500 | 8.55% | 15.25% |

| S&P 500 (equal weight) | 6.90% | 19.18% |

| S&P Mid Cap | 3.64% | 17.59% |

| Russell 1000/Growth | 11.93% | 12.99% |

| Russell 1000/Value | 5.21% | 17.05% |

| Russell 2000 | 4.29% | 17.54% |

| NASDAQ Comp. | 9.68% | 12.92% |

The S&P 500 Index closed the first half of the year at a record high, gaining 15.2% on a total return basis. The first half return was the best in over twenty-two years and represented the fifth consecutive quarter of gains. Stocks were the only asset class with positive returns in the first half as treasury bonds (-7.5%), investment-grade bonds (-1.1%) and gold (-6.8%) all fell. International stocks (MSCI-ACWI-ex US) and emerging markets trailed U.S. stocks gaining 9.4%, and 7.6%, in U.S. dollar terms, respectively. For the first half of 2021, the Russell 1000 Value Index led the Russell 1000 Growth Index by 4.05%, despite the strong outperformance by growth in June of over 740 basis points. For the first half, all eleven of the major S&P 500 sectors posted positive returns. Energy was the standout sector, gaining 42.3%, followed by financials (+24.5%), real estate (+21.7%) and communication services (+19.1%). Market laggards were consumer staples (+3.6%) and utilities (+.79%). Small-cap stocks and mid-cap stocks outpaced the larger companies in the first half despite lagging in the second quarter. As the quarter ended, investors began to weigh whether the recent acceleration in inflation is transitory or the beginning of a longer-term trend that might force the Federal Reserve to become more hawkish.

Growth Strategy

Commentary & Thoughts

Last quarter’s letter discussed our framework of investing in growing companies at reasonable prices. We wrote about what we believed to be unreasonable prices being paid for some growth stocks and unproven entities such as SPAC’S and Software (SaaS) stocks. We also referenced some simple valuation math around similar growth stocks from the late 1990s. The tide has seemingly started to recede as the heady valuations of many growth stocks have started coming back to earth since the end of the first quarter. Some of the market darlings of the beginning of the year, such as Tesla, Shopify and the meme stocks have entered correction territory, somewhat related to what is referred to as “re-opening” trades as there has been some rotation to pro-cyclical companies that should benefit from the re-opening of the economy as the vaccines take hold. Covid-winners, like digital transformation and secular growth stocks, have underperformed.

Speaking of the speculative trading frenzy in the meme stocks, such as AMC Entertainment, one has to be taken back by the quote at the beginning of this letter. We can’t recall such a pointed warning in a prospectus before.

As the U.S. economy normalizes further, we expect solid earnings growth from many companies that were negatively affected during the pandemic period. Future earnings growth for these businesses should be quite good, while virus benefactors, Zoom, Peloton and food delivery companies may suffer somewhat.

Long-time readers of our content appreciate our discipline around prices we pay when investing your capital. We have referenced many times that interest rates have trended down from 14% to 0% for the past 40 years. Doubting that they go negative and considering the high probability interest rates normalize to the ranges seen in the early 2000s (4%-10 year Treasury), P/E multiples should contract. We hopefully are positioned in reasonably priced growing businesses where the earnings growth should overcome most of the valuation compression

Second Quarter Portfolio Activity

We again made no changes to our model portfolio. Trading activity was again light and only involved trimming our position in FedEx and adding slightly to AON in a few accounts. The quarter was busy as usual on the research front as we participated in meetings with management from Raytheon and UPS. We also spent time with our friends from long-time investee Brookfield Asset Management learning about a new private equity fund we are interested in. Connor spent the day with the investment team at Markel as they, along with an investment colleague in New York, hosted an informative virtual conference highlighting some new ideas.

Selling is not easy

After a very successful run in FedEx, we opted to trim back the size of our position. Normally, with a good growing business, we don’t like to trim. However, given the circumstances around FedEx’s valuation, as well as the position size in many accounts, we elected (after much handwringing) to trim back the position.

As often said, the hardest decision in investing is deciding when to sell. In the GARP Focused Opportunity strategy, we find selling or trimming difficult. Researching companies, buying, holding, and selling are all tough with all of the dynamics to consider. With selling, there are unique considerations such as the amount of capital gain you incur, opportunity cost and, Charlie Munger’s dogma of never interrupting compounding unnecessarily. We are also reminded of the quote from the great Peter Lynch, “Selling your winners and holding your losers is like cutting the flowers and watering the weeds.”

When we sell or trim, it can create a variety of potential outcomes, such as, the security we sold continues higher while what we allocated your proceeds to declines. Fortunately, we do not feel compelled to immediately reinvest sale proceeds if there is nothing of intelligent value to buy. If we “top tick our sale (trim at what we think might be the highest point in the cycle and the stock declines afterward), we might find ourselves thinking we are smarter than we actually are and could lead us to lose some of the humility needed to be a successful investor.

Trimming position sizes in portfolios can be a prudent exercise in portfolio and risk management, but selling a model position outright (which we haven’t done in quite a while) typically occurs in the event of four possible scenarios:

- Our thesis regarding the investment has changed.

- The valuation (stock price) gets very overvalued relative to business fundamentals.

- Significant management change or poor capital allocation skill is diminishing shareholders’ value.

- We find a company that is superior to the one we are selling.

Our turnover is typically quite low, approximately 20 to 25%. We have positions in companies that we have owned for many years. We do extensive research on a business and the majority of the time, we get the thesis fairly correct. This leads to longterm ownership.

Phil Fisher, the legendary investor and author of “Common Stocks and Uncommon Profits” had a list of 15 points to be considered when evaluating an investment. He was relentless in adherence to these 15 qualities and felt if he checked all boxes, he would rarely need to ever sell. But mistakes of judgment do happen and it is mostly the price paid at the time, but sometimes the thesis. Fisher writes: “When a mistake has been made in the original purchase and it becomes increasingly clear that the factual background of the particular company is, by a significant margin, less favorable than originally believed… then the proper handling of this type of situation is largely a matter of emotional self-control. To some degree, it also depends upon the investor’s ability to be honest with himself.”

In the case with FedEx, we obviously understand the company well and feel like we know the key fundamentals of the delivery business, including UPS. Our first purchase in 2019 proved to be a little early. But who knew a global pandemic would arrive and dramatically alter all stock prices and yet, enhance the delivery business as brick-and-mortar traditional retail moved online and needed to be delivered? We always knew FedEx was a capital-intensive business given the thousands of planes and trucks they operate, not to mention the massive logistical labyrinth the company faces daily. We never liked the capital allocation to the TNT Express acquisition in Europe and watched as FedEx wrote down our shareholder value for more quarters than we would like to admit. What we did do well was buy a lot more shares at a really good price during the virus selloff of last year. That second purchase has proven to be almost a triple, and coupled with our original purchase, a wonderful return. From a risk management perspective, given the position size in many accounts coupled with the valuation, we painstakingly elected to cut the size back to a normal weight.

Hopefully, Peter Lynch would approve. We cut a few flowers and put them in a vase to enjoy while leaving the garden intact

with little weeding needed.

Contributors and Detractors for Focused Opportunity Growth

Our thoughts on positions that had the most positive impact on the strategy for the period ending 6/30/2021

Danaher (DHR) +19.2%

Danaher’s momentum continues with another quarter of strong top-line revenue and bottom-line profit. Strength in its life sciences and medical diagnostics segments were related to tailwinds from COVID-19 effects. The Danaher business system remains focused on accelerating core growth and margin expansion through innovation.

Charter Communications (CHTR) +18.6%

Charter continues to enjoy its strong competitive position as a leader in delivering high-speed broadband and video. Charter’s cable network has significant competitive advantages versus its primary competitors, telephone companies AT&T and Verizon. Free cash flow this past quarter was $1.9B, up from $1.4B a year ago despite higher capital spending.

Moody’s Corporation (MCO) +18.3%

Moody’s is coming off of its biggest quarter ever with revenue of $1.6B. This strength was driven by higher ratings revenue as new bonds came to market in the leveraged loan arena needing to be rated. Moody’s continues to operate very profitably in its cozy duopoly with S&P. Moody’s is one of our more fully valued (expensive) businesses but offers a strong competitive position.

Alphabet, Inc (GOOG) +17.2%

Google had blowout quarterly earnings on the back of its accelerating core search business and rapid growth in YouTube, Google Cloud and Google Play. We remain solidly invested in Google and we are particularly pleased with the efforts and success the company is having by gaining a stronger foothold in the fast-growing public cloud market.

Wells Fargo (WFC) +14.3%

Wells Fargo continues its turnaround and healing from its reputational damage. We remain optimistic about the potential earnings power over the next several years. This next quarter, we expect to see the regulatory-driven asset cap lifted thereby driving much desired and accretive capital reallocation, especially buybacks.

Our thoughts on portfolio positions that had negative or the least positive impact on the strategy for the period ending 6/30/2021

Dollar Tree (DLTR) -14.2%

Dollar Tree Plus (its new format that includes a section with discretionary items that cost more than the traditional $1 Dollar Tree limit) and its combo stores of Family Dollar and Dollar Tree continue to resonate with customers, driving growth. Headwinds, due to shipping and freight costs (due to shortages) have impacted the shares recently. We believe consumer’s desire for convenience and value continues to position the company for future growth.

Walt Disney (DIS) -7.0%

Disney’s impressive content lineup – including Disney, Pixar, Marvel, Star Wars, ABC, ESPN and acquired FOX content – has enabled the company to be a leader in streaming video. Disney management claims to be on track for over 300 million paid streaming subscribers by 2024. By contrast, Netflix has about 208 million today. We remain very comfortable long-term investors in Disney, notwithstanding its premium valuation.

Verizon (VRZ) -3.9%

Verizon remains well positioned as the wireless leader in network quality and reliability. The company’s large loyal customer base is one of its key investment merits. As 5G becomes a reality in the years ahead, we will pay more for that experience and Verizon should profit. Verizon remains more profitable than its competition due to its efficiency and large market share. We remain long-term investors as long as we stay wedded to our phones.

Abbott Labs (ABT) -2.5%

Abbott is taking a breather as much welcomed relief from the vaccines has impacted Abbott’s COVID-19 diagnostic testing machines. Profitability continues to shine in other areas of the company’s business, such as nutritionals and established pharmaceuticals. We like our future growth prospects as Abbott is investing in heart products such as replacement valves. With 60% of sales occurring outside the U.S., we look for long-term growth continuing.

Mastercard (MA) -0.5%

In our opinion, few companies can match Mastercard’s record of consistent, rapid revenue and earnings growth. Mastercard benefits as consumers reemerge from the pandemic and are spending more on credit, debit and prepaid cards. The company continues to adapt to new trends (including threats), such as mobile payments and virtual cards, while pursuing large new opportunities such as business-to-business transactions. Mastercard is another one of our more expensive stocks.

Classic Value Strategy

Commentary & Thoughts

As markets rise, it is human nature for investors to become more optimistic. As Warren Buffett once stated, it is wise for investors to be “fearful when others are greedy, and greedy when others are fearful.” In reality, the emotions of fear and greed make this more difficult than it might seem for many market participants. A recent survey done by Natixis Investment Managers (6/23/2021), showed that individual investors expect the U. S. markets to increase by 17.3% this year, after inflation. This is on top of a return of 40.8% for the S&P 500 Index over the past twelve months. It is also more than twice the return on U. S. stocks since 1926, which when simply averaged, approximated 7.1% (after inflation) for the entire period.

The CFO Survey, compiled by Duke University and the Federal Reserve Banks of Richmond and Atlanta, found in March 2021 that chief financial officers expect the S&P 500 to return 8.4% annualized over the next decade, up from the 6.8% they predicted back in December 2020. While corporate CFO’s have become more optimistic, it appears less so than expected by individual investors. Clearly, emotions have shifted from “fear,” which was evident as the pandemic began in the first quarter of 2020, to what is likely to be excessive “optimism” today. As the chart below indicates, the S&P 500 trades at 21.5 times forward earnings estimates versus a 25-year average of 16.7 times. The S&P 500 Index dividend yield is 1.44%, well below the 25-year average of 2.02%. Historically, when the markets trade at elevated valuation levels, return expectations would be more muted going forward. Perhaps individual investors need to reign in their optimism.

S&P 500 Index

| Valuation Metric | Latest | 25-Year Average |

|---|---|---|

| Forward P/E | 21.5x | 16.7x |

| Dividend Yield | 1.44% | 2.02% |

| Price/Book | 4.19x | 3.02x |

| PPrice/Free Cash Flow | 16.1x | 10.9x |

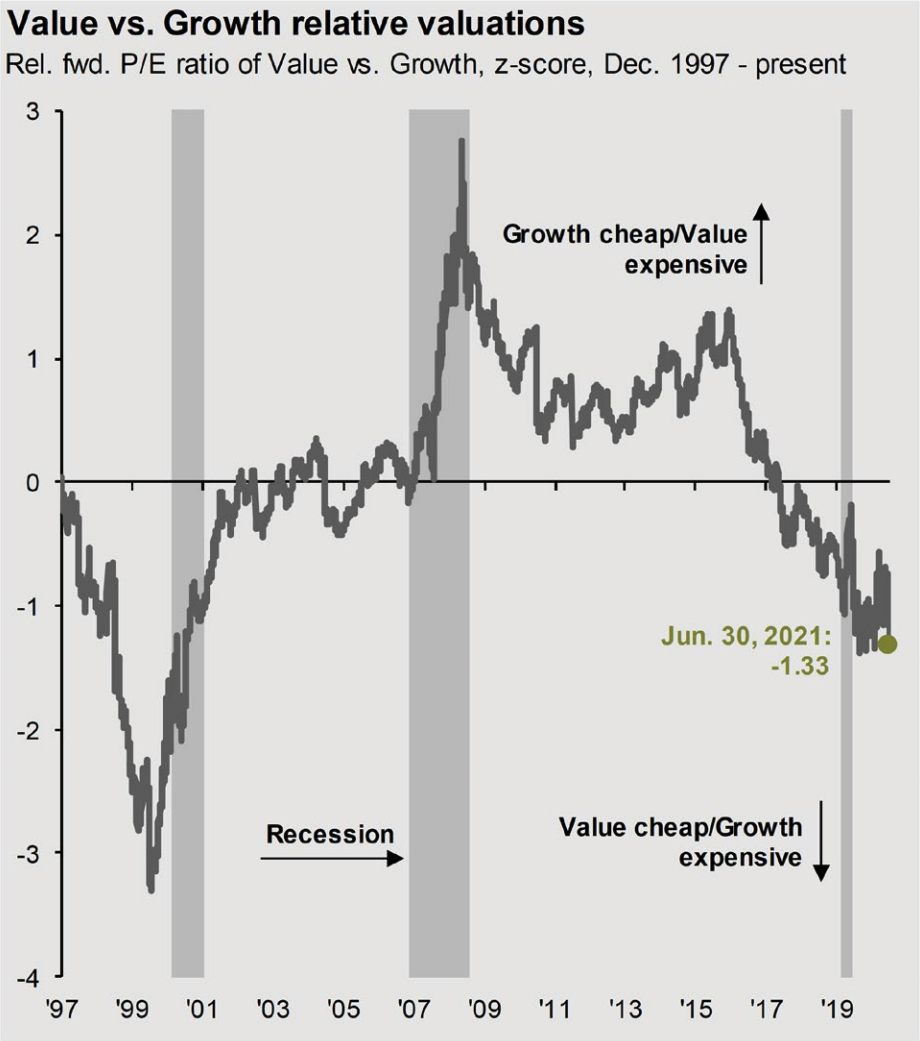

While valuation levels in the market appear elevated on a historical basis, “value” continues to look extremely compelling relative to “growth”. The chart below from J. P. Morgan Asset Management compares the relative forward price/earnings ratio of the Russell 1000 Growth Index to the Russell 1000 Value Index.

Source: FactSet, FTSE Russell, NBER, J.P. Morgan Asset Management

Source: FactSet, FTSE Russell, NBER, J.P. Morgan Asset Management

| Valuation Metric | Russell 1000 Growth | Russell 1000 Value |

|---|---|---|

| Price/Book | 14.0x | 2.7x |

| Dividend Yield | .7% | 1.9% |

| Price/Earnings (ex neg earnings) |

38.1x | 19.5x |

In recent weeks, investors have shifted back to growth strategies, making the case for value (in our opinion) even more compelling. We often remind investors that we think a great company does not always result in a great stock. The price one pays for a security is an integral part of the return the investor ultimately receives. As Benjamin Graham stated, “The margin of safety is always dependent on the price paid. It will be large at one price, small at some higher price, nonexistent at some still higher price.”

Second Quarter Portfolio Activity

During the most recent quarter, there were no new portfolio additions or deletions. We did trim positions in UPS, Invesco and Charles Schwab during the quarter as position sizes became outsized due to strong performance in recent quarters. We remain constructive on each company, but felt on a short-term basis, the shares had met our price objective.

Contributors and Detractors for Classic Value

Our thoughts on positions that had the most positive impact on the strategy for the period ending 6/30/2021

United Parcel Service (UPS) +21.4%

UPS is the world’s largest express carrier and package delivery company. UPS’s earnings momentum continued in the most recent quarter with domestic average daily volume growing by 12.8% to 20.4 million packages per day. Under the leadership of new CEO Carol Tome, we expect UPS to be successful in removing $500 million in nonoperating expenses over the next several years.

Roche Holding (RHHBY) +15.3%

During the most recent quarter, sales of COVID-19 tests helped to offset weakness in the drug business, as the pandemic limited doctor visits for other diseases. Recent strength in the share price is likely due to rumors that Roche will seek early FDA approval for Alzheimer’s disease candidate Gantenerumab.

Alphabet (GOOGL) +14.7%

Alphabet’s first quarter revenues surged 34% largely due to increased advertising spending by its customers. We believe GOOGL remains attractive and trades at a discount to the “sum of the parts”, which Sanford Bernstein estimates could be as high as $3,100 per share. Alphabet has a rock-solid balance sheet with $137 billion in cash, versus $14 billion in long-term debt.

Diageo (DEO) +14.5%

Diageo is a London based spirits company with popular brands such as Johnnie Walker, Bailey’s, Captain Morgan, Crown Royal, Smirnoff and Guiness Beer. In an update on May 12th, the company stated they saw strong growth across all regions. While DEO shares are no longer priced cheaply like they were in the pandemic, the company has a unique competitive position “moat” that in our opinion, could not be easily duplicated.

CVS Health (CVS) +12.3%

In the past quarter, CVS reported results that were ahead of analysts’ forecasts. CVS shares currently trade at approximately 10 times forward earnings while the S&P 500 trades at 21 times. CVS shares yield 2.4% versus 1.4% for the S&P 500. Despite the recent move, we believe CVS shares represent good value.

Our thoughts on portfolio positions that had negative or the least positive impact on the strategy for the period ending 6/30/2021

Dollar Tree (DLTR) -14.2%

Despite reporting earnings that were in line with expectations, Dollar Tree shares have been weak as fears of cost pressures (labor and freight costs) have weighed on the stock. The new concept that combines Dollar Tree and Family Dollar brands has been promising and are expected to drive a same-store sales lift. Long-term debt, which peaked at $7.3 billion at the time of the Family Dollar acquisition has been pared to $3.2 billion and should continue lower. Dollar Tree shares trade at approximately 16 times earnings versus 20 times for competitor Dollar General. We think the shares remain attractive for investors.

Intel (INTC) -13.0%

Intel’s appointment of Pat Gelsinger as CEO in February was initially met with enthusiasm, however to us, the honeymoon period appears to now be officially over. Intel’s earnings will likely decline over the near term, however, Gelsinger has exciting plans to “redouble on manufacturing” so that Intel regains its competitive edge. Intel shares appear attractive as they trade at only 11 times earnings (versus 38 times earnings for the SOXX semiconductor index) and yield 2.5%.

Fiserv (FISV) -12.5%

Fiserv provides internet banking, bill payment credit card processing and risk management to 18,000 financial institutions. Fiserv’s first quarter earnings exceeded analysts’ expectations while revenues were slightly behind projected numbers. The company benefited from good organic growth, particularly subsidiary Clover, whose revenues were up 36%. Growing cash flows should allow for deleveraging following the purchase of First Data in 2019.

Sony (SONY) -9.0%

In the most recent quarter, Sony reported a record net profit, with earnings largely driven by the Playstation division. The recent report was cautious going forward due to projected declines in music and games. Sony’s finances are strong with cash and equivalents standing at over $41 billion, while debt only represents 17% of total capital. In our opinion, Sony has excellent long-term prospects with dominant positions in gaming, music, pictures and semiconductors.

Walt Disney (DIS) -7.0%

Disney is well positioned for a near-term rebound as the theme park business recovers from the Covid 19 shutdown. The shares’ recent pullback has largely been attributed to the fact that Disney+ signed on less than expected new users in the most recent quarter. Keep in mind Disney+, at quarter end, had 104 million subscribers which is incredible over an eighteen-month period.

International Strategy

Commentary & Thoughts

U.S. developed markets continue to outperform this quarter relative to the rest of the world, especially Asia. We remain cognizant of strained U.S. and China relations. We believe the incentives for the Chinese government to promote economic growth remain strong. We are closely watching globalization in general as the movement of goods and services around the world has been called into question with the pandemic. Global low-cost logistics have been deflationary in the past. If large chunks of U.S. production in Asia move back to the U.S., Canada and Mexico to better endure more trustworthy supply chains, the ramifications could be more inflationary

We receive occasional questions from clients regarding our positions in Chinese stocks. We wouldn’t claim to fully appreciate all the Chinese geopolitical risks that are apparent, but we are comfortable with what we own, notwithstanding the weakness this quarter.

Our comfort comes from Bloomberg data that reports that Asia accounts for 60% of the world’s population and is forecasted to contribute 60% of the world’s economic growth over the next decade, in large part because 90% of 2.4 billion estimated new members of the middle class are from Asia. According to Bloomberg, Asia’s share of global GDP was around one third in 2000, reached 40% in 2020 and is forecast to be 50% by 2040.

China is the driving force in Asia. Its economy continues to evolve from an export-driven focus to more of a consumer led one. The wealth creation in China has been remarkable and we believe it should continue to materially outpace the rest of the world on that measure.

Export-driven Europe stands to benefit from calmer foreign trade policies. Brexit for now “is what it is” and the end of this uncertainty could unlock some real investment into European supply chains. Europe could possibly be more of a coiled spring than many expect and with pent-up demand, consumer resilience, and increased savings now in the forefront, there could be several years of robust growth ahead. Pre-pandemic, Europe was a market that was ripe for special situations such as activism, M&A, breakups and spinoffs. One of our key portfolio positions, Vivendi, announced just this sort of thing with its pending spinoff of Universal Music Group. We believe this should unlock significant shareholder value.

Live Oak Private Wealth International Portfolio Activity

We made no model changes to the International strategy. The only portfolio activity was buying and taking New Oriental Education to a full model weight position in all global model accounts.

We keep doubling down on our research efforts, making sure we appreciate the risks New Oriental Education faces as the Chinese government is implementing additional regulations on online education companies, which has heightened the uncertainty and weighed tremendously on the stock price. The Chinese are extremely focused on education and the acceptance rates to the top schools in China are much lower than the rates at comparable schools in the U.S. New Oriental’s primary business is after-school tutoring, preparing students for the extremely rigorous high school and college entrance exams. The stock has pulled back a lot more than we expected as any and all growth has been called into question and there is a tremendous amount of uncertainty. We feel like this has created an opportunity for patient investors like us. The P/E multiple was too high going into this uncertainty with heightened government regulations. If you subtract the net cash on the balance sheet from the current market cap, EDU trades for 15x our earnings estimate for next year. Founder, Michael Yu is the largest shareholder with an 11.5% stake worth $1.4B, down from over $3.0B. He has been an excellent steward of the company’s capital in the past and hopefully, he can help to navigate us through this temporarily uncertain time, which has created this opportunity.

Contributors and Detractors for International Strategy

Our thoughts on positions that had the most positive impact on the strategy for the period ending 6/30/2021

Heineken (HEINY) +16.7%

Heineken continues to build back business that was lost due to the pandemic shutdown. Europe has been a little slower to open up, but bars and restaurants are coming to life and from our perspective, Heineken’s namesake brand is well positioned to gain market share. We remain content investors as the company is not letting a crisis go to waste by planning on $2B euro-cost containment endeavors to expand margins further. Heineken is the world’s second-largest brewer.

Roche Holdings (RHHBY) +15.3%

Roche’s drug portfolio and industry-leading diagnostics continue to strengthen the company’s competitive advantages. The Swiss healthcare giant is in a unique position to guide global health care to a safer, more personalized and more cost-effective endeavor. Blockbuster cancer biologics, Avastin, Rituxan and Herceptin are big revenue drivers. The company’s U.S. arm, Genetech, has solid important therapies in oncology. We like the long-term prospects for Roche.

GVC Holdings (GVC) +13.6%

GVC, now known as Entain, is an international sports betting and gambling company. The company’s gaming operators operate through both online and retail channels. The company is growing rapidly through M&A and organic growth emanating from tremendous demand for sports betting as many U.S. states move to legalize sports wagering. We believe Entain’s new collaborative venture with BetMGM will most likely unlock significant growth opportunities.

Phillip Morris International (PM) +12.6%

Phillip Morris continues to innovate and develop reduced risk cigarette products. The company is purposedly disrupting its own legacy combustible cigarette business with its new IQOS product. This “heat not burn” cigarette uses a technology-enhanced device that positions Phillip Morris as a first mover in heated tobacco. With 28% global market share and over a 4% dividend yield, we are comfortable investors.

Ferguson (FERG) +12.3%

As the world’s leading distributor of plumbing and heating products, Ferguson is benefitting from tremendous growth due to new housing construction and pandemic stay-at-home renovation projects. U.S. market demand continues to accelerate as the U.S. economy fully reopens. Recent quarterly revenue of $5B was a 24% increase over last year. As more and more new households are formed and housing remains robust, we are bullish on Ferguson.

Our thoughts on portfolio positions that had negative or the least positive impact on the strategy for the period ending 6/30/2021

New Oriental Trading (EDU) -43.5%

New Oriental’s stock price continues to be very weak in the face of significant new regulations placed on Chinese online education companies. There is tremendous uncertainty weighing on this sector and selling pressure hasn’t abated. As long-term investors, we are sticking with New Oriental as we feel that they are the market leader in this educational niche and therefore, can endure this uncertain period and respond to the government’s new protocols.

GAN LTD (GAN) -15.1%

GAN is an award-winning provider of enterprise Software-as-a-Service (SaaS) solution for online casino gambling, commonly referenced to as iGaming, and online sports betting. Online sports betting is a rapidly growing industry as many U.S. states legalize sports wagering. GAN offers an internet gaming ecosystem platform that is helping the brick-and-mortar casino industry transform to digital. GAN is our smallest company in our portfolio with annual revenues of $110mm. Potential rapid growth lies ahead and we are opportunistic about the company’s growth prospects.

Ten Cent Holdings (TCEHY) -10.2%

Ten Cent Holdings’ WeChat application is the dominant messaging platform in China. The company continues to use this dominance to position itself in many new growth areas such as payments, video and music streaming, and online advertising. Tencent is also the leader globally in video games. The stock, like most of the Chinese stocks this quarter, was weighed down by new, unpredicted regulations emanating from the Chinese government. We remain comfortable with the company’s future growth prospects.

Daikin Industries (DKILY) -8.9%

Daikin is a large Japanese conglomerate. Our stock thesis resides with Daikin North America, which is a global leader in HVAC applications. The company’s commitment to air filtration and elevating the quality of air in homes, businesses and public spaces gives us comfort in growth ahead. Now post-pandemic, all of us are laser-focused on virus-free clean air and Daikin is positioned to address this need. New subscription-based programs for monthly air filter replacements bode well for the company’s affiliate, American Air Filter Company in Louisville, KY.

Baidu.com (BIDU) -7.2%

Baidu is the Google of China. Founded as a search engine platform, Baidu is now a leading artificial intelligence company with a strong internet foundation. Baidu provides a large suite of online marketing services which continue to grow handsomely. Like many of our other Chinese tech companies, Baidu has been weighed down by heightened concerns of increased regulations by the Chinese government. Over time, we feel this uncertainty will abate and the shares will respond favorably to the business growth that hasn’t slowed.

Final Thoughts

Our team spends a lot of time honing our processes to improve our decision-making and hopefully your outcomes. One of our endeavors is studying and researching different frameworks that can position us to make better decisions. Frameworks need to adapt and evolve so that in building and managing investment portfolios, we actually see the great opportunities when they come along. The key to our framework is deep thought or mindfulness. We try to have eyes wide open and awake and be aware of the changing environment around us. Purposely being mindful crafts better behavior and decisions that set us up for better investment results.

Mindfulness is not brain surgery, it is just the disciplined act of paying closer attention. It sounds so simple, but it is difficult in today’s distracted world. The brain is wired to work against us in today’s modern environment of mobile phone notifications, texts, email and open offices, etc.

Time is an important element in mindful decision-making. If we don’t structure quiet focus time for research, opportunities will pass us by. We attempt to allocate our time for careful study with the same consciousness as we allocate the hard-earned capital you have entrusted to us. We try hard to not let our brains be bombarded with noisy information emanating from CNBC and Twitter or constant email, texts and unnecessary meetings. We strive to create time and space to find signals increasingly buried in the information deluge around us daily to make mindful, and hopefully profitable, decisions. We look at our portfolios constantly and ask what is unlikely to change over the next decade or longer and then position all of us in those best opportunities. Careful attention and concentration allow us the free time and space to connect dots when opportunities present themselves. We perceive this framework as one of Live Oak Private Wealth’s competitive advantages.

Thanks to you, our clients, Live Oak Private Wealth continues to grow. We always felt that our unique value proposition was a winner and would resonate with clients. We couldn’t be happier as we close in on September 1st, our three-year mark. To leverage our growth and future success, we are excited to share with you two new members of Live Oak Private Wealth. Laura Tayloe joined the team the 1st of May and Angel Bolton will start the 1st of August.

Laura Tayloe joins the Live Oak family as our client experience specialist. Her role will be to ensure all of our team is delivering and executing on the best possible experience you as a client receives and deserve. Laura joins us from Mainstone Capital Management in Boston and Windhorse Capital Management, a multifamily office in Boston as well as The Carlyle Group.

Angel Bolton, CFP®, joins the Live Oak family as our second fiduciary planner. Her role will be to leverage our existing extensive suite of financial planning, trust and estate capabilities on behalf of our clients. Angel joins us from the private bank division of Wells Fargo and will initially work closely with the Rocky Mount team helping them solve the many trust, tax and estate planning needs today.

Live Oak Private Wealth has been blessed from its beginning to have a solid core of very valuable service specialists, Missy Musser and Amy Bennett. Strengthening us further was the addition of Jan Robbilard and Terry Sapp, who were instrumental in Jolley Asset Managements success. Now we are very fortunate to be able to have two new qualified, delightful and professional ladies join our team. We encourage you to reach out to each of them and say hi.

Bill and the Wilmington team would also like to point out that June 30, 2021 marks an important milestone. Frank Jolley and his Rocky Mount team built a highly regarded, trusted and successful investment firm in Jolley Asset Management over 20 years ago. As Jolley Asset Management and Live Oak Private Wealth join together, Jolley’s legacy of trust, integrity, service to the client and stellar investment results lives on. The commitment to be a true fiduciary, acting daily to always do what is in the client’s best interest, lives on. So, while the name on the door in Rocky Mount might look different, what’s inside will not. Our overall value proposition has been strengthened by the addition of Frank, Bill, Terry and Jan and we couldn’t be prouder to partner with them.

“We don’t know.” This is generally our answer to the regular questions posed to us about our macroeconomic, geopolitical and market views. Whether inflation is transitory or not, when the Fed will taper and will capital gain tax hikes be retroactive are all questions we can’t answer. What we can say is that we will continue to research and hopefully find reasonably priced businesses with the hopes that they will be incremental to our portfolios.

Stocks continue their march higher, ignoring the cyclical nature of the financial markets for now. We remain very cognizant and aware of the tremendous bullish sentiment against a myriad of uncertainties. We continue to manage your wealth as we do our own, with an ample margin of safety. We are grateful and appreciative for our partnership with you and your willingness to compensate us for doing something we love to do and is so important to us all.

Our entire (and growing) Live Oak Private Wealth Team looks forward to our continued shared success together.

With warmest regards

Co-Chief Investment Officer

Co-Chief Investment Officer

Disclosures

- Past performance is no guarantee of future results and future performance may be higher or lower than the performance shown. The performance results for each equity sleeve are calculated for us by Orion Services and does not reflect investment management fees, custody and other costs or taxes. All of which would be incurred by an investor in any account managed by Live Oak Private Wealth.

- The performance attribution represented is a simple point-to-point price percentage change for the five best and five worst portfolio positions for the third quarter ending September 30, 2020 Each equity sleeve does not and is not intended to indicate past or future performance for any account or investment strategy managed by Live Oak Private Wealth. Additionally, there is no guarantee that all portfolios will own any or all of the companies mentioned.

- There can be no assurance that our portfolio management or any account managed by our investment managers will achieve a targeted rate of return or volatility or any other specified parameters. There is no guarantee against loss resulting from an investment.

- Investment objectives, returns, and volatility are used for measurements and/or comparison purposes only and are only a guideline for prospective investors to evaluate our investment strategy and the accompanying risk/reward ratios.

- Comparison to any index is for illustrative purposes only. Certain information, including index and benchmark information, has been provided by third-party sources, and although believed to be reliable, has not been independently verified and its accuracy cannot be guaranteed.

- The information contained here is not complete, may change, and is subject to, and is qualified in its entirety by, the more complete disclosures, risk factors, and other important information contained in Part 2A or 2B of Form ADV. This presentation is for informational purposes only and does not constitute an offer to sell or as a solicitation.

- Live Oak Private Wealth is a subsidiary of Live Oak Bank. Investment advisory services are offered through LOPW, LLC, an Independent Registered Investment Advisor. Registration does not imply a certain level of skill or training.

- Opinion and thoughts expressed are those of Bill Coleman and Frank Jolley and not Live Oak Bank.

- Not all portfolios will necessarily own all companies mentioned, due to factors such as legacy positions, capital gain constraints, sector concentration, time, and other considerations.