Get Live Oak Private Wealth’s perspective on the shifting investment patterns and the impact on clients by downloading our 2024 Year-End Letter.

“It shouldn’t come as a surprise that the return on investment is significantly a function of the price paid for it. For that reason, investors clearly shouldn’t be indifferent to today’s market valuations.” – Howard Marks

Get Live Oak Private Wealth’s perspective on the shifting investment patterns and the impact on clients by downloading our 2024 Year-End Letter.

Tax policy and the temporary or “sunsetting” provisions of the 2017 Tax Cuts and Jobs Act (TCJA) have become a large focus of the 2024 U.S. presidential election.

Tax policy and the temporary or “sunsetting” provisions of the 2017 Tax Cuts and Jobs Act (TCJA) have become a large focus of the 2024 U.S. presidential election. It’s important to understand that on December 31, 2025, this “sunset” expires several tax benefits (including the increased gift, estate and GST tax exemptions) of the TCJA unless Congress passes legislation. For an in-depth description of specific TCJA expiring tax provisions, see Table I included in CRS Report R47846, Reference Table: Expiring Provisions in the “Tax Cuts and Jobs Act” (TCJA, P.L. 115-97), by Margot L. Crandall-Hollick, Donald J. Marples, and Brendan McDermott at (https://crsreports.congress.gov/product/pdf/R/R47846).

How do election outcomes impact tax policy?

For the temporary provisions of the TCJA to be extended or modified, Congress must act. Typically, the biggest policy advancements occur when one party controls the White House and both houses of Congress. In addition to the Presidential race, a total of 468 seats in the U.S. Congress are up for election in November. That includes 33 of the 100 seats in the U.S. Senate (currently under narrow Democratic control) and all 435 seats in the U.S. House of Representatives (currently under narrow Republican control). Whether the election outcome results in one-party control of both houses of Congress and the Presidency, or a split between the parties as exists today, is yet to be seen.

At the presidential level, the candidates continue to issue additional tax policy details as the election approaches. You can stay up to date on tax policies proposed by presidential candidates by visiting the Tax Foundation’s “Tracking 2024 Presidential Tax Plans” resource page at https://taxfoundation.org/research/federal-tax/2024-tax-plans/

What are some of the potential impacts of “sunset” or extension of the TCJA?

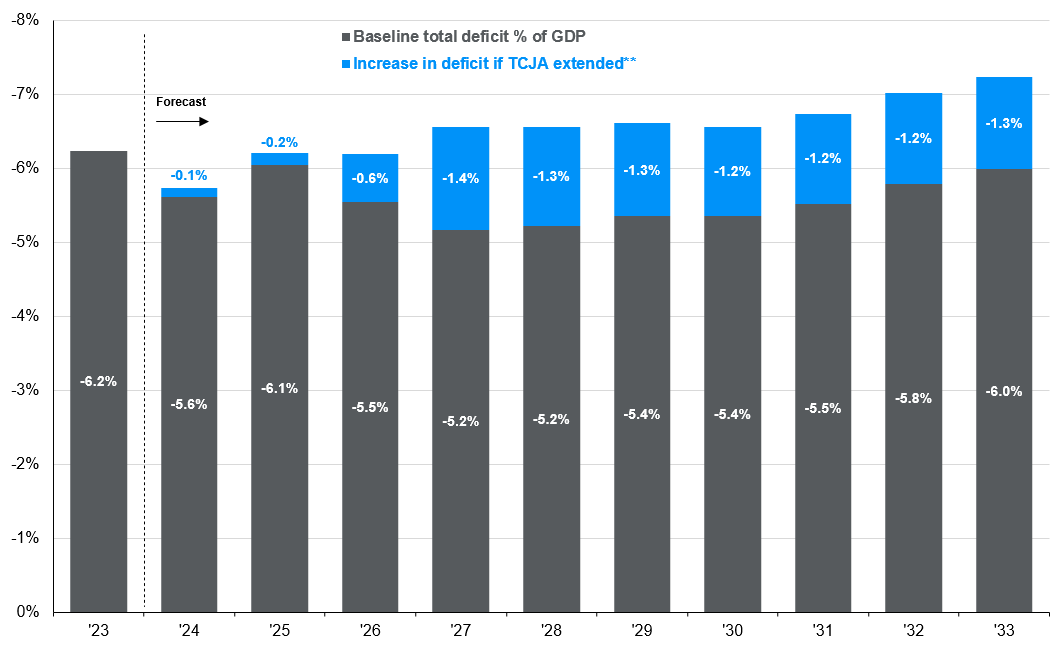

Under current law, the Congressional Budget Office (CBO) projects individual tax revenue to increase after 2024 because of the expiration of tax cuts under the temporary TCJA provisions. If the individual tax provisions are extended, this would create new federal budget deficit concerns from the resulting tax collection reduction (an estimated addition of $2.6 trillion to the federal debt through 2033 – $2.5 trillion from individual tax rate changes and $126 billion from estate tax exemption changes). If the TCJA tax cuts “sunset” and the taxpayers’ bills increase by $2.6 trillion over the next decade, this could impact consumption and consequently growth. This tension is what makes the policy decision delicate and difficult.

Increase in federal deficit if the Tax Cuts and Jobs Act (TCJA) is extended*

% of GDP, 2024 – 2033, impact based on CBO Baselines Forecast Source: CBO, J.P. Morgan Asset Management. *Estimates are based on the Congressional Budget Office’s (CBO) “The Budget Outlook and Economic Outlook: 2024 to 20234.” **Assumes the following provisions from the TCJA are extended: changes to individual income tax provisions, higher estate and gift tax exemptions, changes to the tax treatment of investment costs, and maintaining certain businesses tax provisions going into effect in 2023.

Disclosures:

The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass.

Live Oak Private Wealth is a subsidiary of Live Oak Bank. Investment advisory services are offered through LOPW, LLC, an Independent Registered Investment Advisor. Registration does not imply a certain level of skill or training. More information about Live Oak Private Wealth, including our advisory services, fees, and objectives, can be found in our ADV Part 2A or 2B of Form ADV, which is available upon request.

Read our full investment commentary and letter to clients by downloading the Q3 2024 quarterly letter.

“October: This is one of the peculiarly dangerous months to speculate in stocks. The others are July, January, September, April, November, May, March, June, December, August, and February.” -Mark Twain

What a difference a year can make in the capital markets! As we were writing the 2023 Q3 newsletter last year, it felt like chaos was reigning in the stock and bond markets.

Read our full investment commentary and letter to clients by downloading the third quarter 2024 letter.

Read our full investment commentary and letter to clients by downloading the 2024 Mid-Year letter.

“Reaping dependably high returns from risky investments is an oxymoron. But there are times when this caveat is ignored—when people get too comfortable with risk and thus when prices of securities incorporate a premium for bearing risk that is inadequate to compensate for the risk that’s present.”

-Howard Marks

The second quarter of 2024 saw mixed results for the equity markets as strength continued in mega-cap technology companies, while the rest of the market languished. Massive spending on artificial intelligence has sent the Magnificent Seven (Microsoft, Apple, NVDIA, Alphabet, Amazon, Meta, and Tesla) soaring, and they now make up a whopping 32.8% of the S&P 500 index. Despite the lofty valuations in the Magnificent Seven, investors and algorithmic programs are piling in at the expense of the remaining 493 companies where economic growth appears to be slowing. This has resulted in the third narrowest six-month period ever, with only 24% of stocks in the index outperforming the S&P 500 index.

Read our full investment commentary and letter to clients by downloading the 2024 Mid Year letter.

Read our full investment commentary and letter to clients by downloading the Q1 2024 quarterly letter.

“The desire to perform all the time is usually a barrier to performing over time.” – Robert Olstein

As 2023 drew to a close, speculation around Fed Chairman Jerome Powell’s comments on potential rate cuts fueled a strong rally. The momentum continued into the first quarter of 2024, resulting in gains across all equity indices. However, the attitude towards interest rates now seems to suggest that rates will be higher for longer and how that will influence the market returns remains to be seen in the year ahead.

Read our full investment commentary and letter to clients by downloading the first quarter 2024 letter.

Get Live Oak Private Wealth’s perspective on the shifting investment patterns and the impact on clients by downloading our 2023 Year-End Letter.

“Develop into a lifelong self-learner through voracious reading; cultivate curiosity and strive to become a little wiser every day” – Charles T. Munger (1924-2023) Vice Chairman | Berkshire Hathaway

Get Live Oak Private Wealth’s perspective on the shifting investment patterns and the impact on clients by downloading our 2023 Year-End Letter.

Read our full investment commentary and letter to clients by downloading the Q3 2023 quarterly letter.

“Patience and discipline can make you look foolishly out of touch until they make you look prudent and even prescient.” -Seth Klarman, The Baupost Group

“Nothing like price to change sentiment.” -Helene Meisler

As we write this 3rd quarter letter, we are and have been experiencing several major headwinds for the US economy and the US equity and bond markets. While this is nothing unique to investors and markets, it seems as if an abnormal number of issues are at the forefront of markets.

Read our full investment commentary and letter to clients by downloading the third quarter 2023 letter.

Read our full investment commentary and letter to clients by downloading the Mid-Year letter.

“The best way to measure your investing success is not by whether you’re beating the market but by whether you’ve put in place a financial plan and a behavioral discipline that are likely to get you where you want to go.”

-Benjamin Graham

Any number of things could have derailed the equity markets in the first six months of 2023. Despite a banking crisis, the threat of a U. S. debt default, and more rate increases from the Federal Reserve, the markets climbed a “wall of worry” with the S&P rising by 16.9%. Investors have been encouraged by the fact that the Fed’s rate increases haven’t ended the economic expansion. First quarter GDP increased at a rate of approximately 2% annualized, above the consensus estimate of 1.3%. About the time of the Silicon Valley bank collapse, investors’ attention shifted back to the old leaders, mega-cap technology. Mega-cap tech companies have fortress balance sheets and would likely be less impacted by tightening credit than other areas of the market. More importantly, mega-cap tech companies are expected to benefit from artificial intelligence (AI), which overnight, became all the rage and focus of the markets.

Read our full investment commentary and letter to clients by downloading the Mid Year letter.

You are about to leave the Live Oak Private Wealth website.

Disclaimer: This link will take you to a website outside of the Live Oak Private Wealth site. The new site may offer a different privacy policy and level of security. Live Oak Private Wealth is not responsible for the products or services that are offered or expressed on other websites.