To enjoy and benefit from life-changing gains in the markets, you have to have patience. Read more about the financial benefits of patience.

Author Archives: Bill Coleman

The year 2020 was a prime example of how difficult forecasting financial markets can be. Learn why investing with a margin of safety is so important–and why it drives everything we do.

Download the full first quarter 2020 letter to learn more about Live Oak Private Wealth’s portfolio activity, performance characteristics and comments from the team.

Introduction

“To buy when others are despondently selling and to sell when others are greedily buying requires the greatest fortitude and pays the greatest reward.”

– Sir John Templeton

Unprecedented

un·prec·e·dent·ed

Adjective, without previous instances never before known or experienced; unexampled or unparalleled: an unprecedented event.

– Merriam-Webster

“If you are going through hell, keep going.”

– Winston Churchill

These letters are never easy to write. I wouldn’t have imagined just a few short weeks ago, I would be writing about the swiftest bear market to affect us in modern-day market history, 23 days to be exact. The S&P 500 crashed 30% almost in a straight line over the course of 13 trading days. This has been a painful period for our portfolios. There are many sayings in the investment community and a couple of them resonate currently. One saying is “risk happens fast” and another one is that stocks “take the stairs up and the elevator down.” This recent scenario is another sharp reminder that actual risk is the highest when perceived risk is the lowest. We spent the first month of the quarter enjoying the spillover from a marvelous year in 2019. Everything that seemed so certain has vanished. Numerous valuation metrics were near all-time highs, but the trade war was settling down, there was some clarity around the Democratic race for president and expectations were bright. Risk happens fast.

Countless lives and financial markets have been completely turned upside down over the course of just a few weeks. We, as many did, failed to have the imagination needed to quantify a risk such as a global viral pandemic. No one envisioned something that would cause the global economy to come to almost a full stop. Who would have ever contemplated travel bans from Europe, an empty Times Square, NCAA March Madness canceled and children home from school for the rest of the semester? Shelter in place…no more than 10 people together, beaches closed…virtual Zoom everything…this has all been hard to process.

Thankfully, I can report that all of the Live Oak Private Wealth team is healthy and functioning. While we are dispersed in our respective shelters, we are operating at near 100%. Live Oak was already accustomed to working remotely when needed and with our state-of-the-art cloud based technology, our team hasn’t missed a beat, except personally seeing each other daily. We built Live Oak Private Wealth with strong operational, trading and compliance infrastructure. During these extremely volatile days of thousand point moves in the markets, we managed the portfolios just as if we were in the office. But we, like you, can’t wait to get back to normal. Additionally, we have long-standing “disaster recovery” procedures. Our ability to access client information securely, work with third parties to effect transactions and/or money movement and actually “do investment work” is undiminished amidst the chaos.

History does not always repeat, but it does rhyme as Mark Twain stated. Studying stock market history shows that over a long period of the last century, there have been three types of catastrophic events that have greatly disrupted markets and triggered large declines.

- Economic Catastrophes: The financial crisis of 2008-2009, The Depression in the 1930s and the stagflation of 1974-1975.

- Social Catastrophes: World wars, the terrorist attack of September 11th.

- Financial Market Structure Catastrophes: The crash of 1987, the flash crash in 2010 and the bursting of the .com bubble in 2000.

Now we seem to have a fourth type of catastrophe affecting the markets negatively…a global natural health disaster, COVID-19. This type of coronavirus is unique and a novel event in stock market history. We have never seen a global natural disaster that has led to most all economies in the developed world shutting down in near unison. This is without precedent. Historically, economic catastrophes like the depression and the 2008-09 crisis led to large-scale disruptions and much long-term permanent impairment to value. Financial market structure catastrophes usually recover in due time without much permanent impairment to stock values. Since this scenario is so novel, it is hard to predict the range of outcomes, timing and winners and losers.

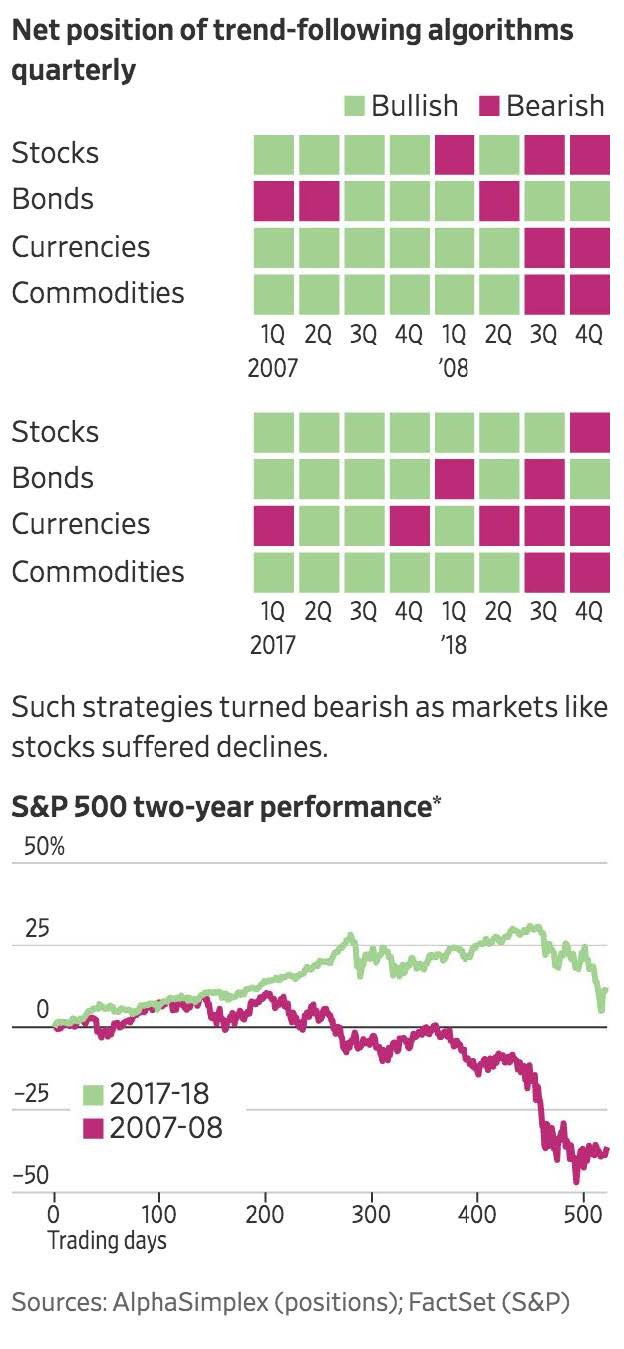

So I want to go back to the 23 day, warp speed bear market for a minute. I want to revisit my soapbox regarding the risks that were inherent in the popular computerized quantitative factor strategies. I don’t want to diminish the significance of the unplanned pandemic and a justified correction, but there were significant technical factors at play here. Market volatility, or VIX in our world, creates massive selling (and buying at times) that is fueled by hedging and trading strategies that reside inside Wall Street “black boxes” or computers. I’m not going to begin to explain “short-gamma positioning” because I don’t even fully understand it, but this type of paradoxical trade is crazy to this old, simple investment manager. This momentum-driven trade buys stocks when they are rising and sells them when they are falling. You read that right. Data provider SqueezeMetrics estimated that tens of billions of dollars of S&P 500 futures had to be sold for every percentage point the S&P 500 went lower during the last week of February. Last I checked, the more something declined in price or went on sale (think steaks, airfare, your favorite shoes) the more prone you were to buy because of the great value.

Shelby Davis, noted value investor, said years ago, “You make most of your money in a bear market, you just don’t realize it at the time.” None of us welcome fear and panic, but we like the bargains that are presented. Buying pieces of really good businesses on sale is rare and it’s valuable. Rational investors buy really good businesses after prices have declined, they do not sell. The lower the price paid for a good stream of company earnings, the higher the future returns available. Investing 101.

Emotion — Panics — Pendulums

Prices of stocks in our portfolios have temporarily diverged from their business values. The current prices reflect the extreme emotions of this moment. They are not careful appraisals of sustainable business value. One of the most significant factors that holds back investors’ success is their tendency to assess the world with emotionalism rather than rational objectivity. During extreme emotionally scary periods like we are in, investor psychology rarely allows us to equal weight positives and negatives. We are biased to the moment. We don’t understand why investors have such short-term memories or why we suffer from recency biases, but we have seemed destined to do so. Consider these hindsights:

| October 19, 1987 | Black Monday market crash saw the Dow drop more than 20% in a single day. |

| January, 1994 | The great bond market massacre which triggered more than $1 trillion in losses. |

| October 27, 1997 | The Dow plunged 550 points (-7%) due to the Asian financial crisis. |

| August, 1998 | Russia defaulted triggering the failure of Long-Term Capital Management and the first Federal Reserve bailout of a corporation or entity. |

| September 11, 2001 | Markets were closed for four days after the 9/11 terrorist attacks and fell -7% when markets reopened. |

| August, 2011 | U.S. Government debt downgrade, triggering -17% stock declines, bank stocks -40%. |

All of these panic selloffs, in just my career, proved to be great opportunities to invest. I would imagine we will look back on this time in a few short years and feel the same. All panics seem to wind up in hindsight as mini panics in history. I’m constantly reminded each time there is a major selloff by the timeless words of wisdom from the great Peter Lynch, who managed Fidelity Magellan, “The key to making money in stocks is not getting scared out of them.”

Investors rarely maintain objective, rational and neutral positions during panics. They are either highly optimistic, greedy and risk tolerant or pessimistic, fearing everything and avoiding risk. In the world of investing, human emotion and perception seem to swing from flawless to hopeless. Noted investor Howard Marks refers to a pendulum that swings from one extreme to another, spending little time in the middle. Emotion is one of the investor’s greatest enemies. You must try to control your inner pendulum of human emotion and minimize error by remaining as balanced or neutral as possible during difficult times such as these.

Portfolio(s) Discussion and Commentary

Our investment team manages three equity portfolios in addition to our fixed income solutions. Each of these three equity portfolios are unique with different approaches. Please see individual commentary at the end of this letter.

- Focused Opportunity

- Select

- International

To say the investment team was busy this quarter would obviously be an understatement. January and early February saw us scouring hundreds of analysts research reports and sitting in on numerous conference calls. We attended several analyst days from portfolio companies. We made our annual trip to Columbia Business School on February 7 for their investment conference. We caught up and visited with other portfolio managers in New York we trust and admire. We discussed the bear market in energy stocks among other things. In the 36 hours we spent in New York with several managers and a day long conference, there was no talk or worry about the risks of a global pandemic such as the coronavirus. Airplanes, hotels and restaurants were packed. There was no sense of insecurity…including yours truly.

Before the selling really accelerated in late February and March, we made two significant decisions in our Focused Equity Portfolio. After much debate and hand-wringing we elected to trim our long-held position in Apple. We just felt that sentiment had become overly optimistic and the valuation was elevated. We opted to sell almost half of our position. Connor was finally able to convince me to sell General Motors after holding it for roughly five years with no real performance to show for it, except for dividends. He has been spot on about peak auto and I should have listened to him earlier. So in hindsight now…those were two good trades.

We started buying meaningfully when the heavy selling started in early March. It is not easy buying stocks when they are falling. The entire Private Wealth team spent a lot of time supporting each other and debating cash levels in accounts and asking if we were buying too soon. Prices were getting cheaper by the day and therefore, the relationship between price and intrinsic value was widening. We knew we couldn’t time the bottom as it can only be recognized in retrospect.

Our main objective was to upgrade the portfolios and add quality where we could. We wanted to further concentrate in our highest conviction businesses while they were on sale. We therefore:

- Bought Wells Fargo on February 28th

- Added significantly to Disney on March 10th

- Added to Markel on March 11th

- Added to Mastercard on March 11th

- Added to Berkshire Hathaway on March 12th

- Bought Exor on March 16th

- Added to Microsoft on March 17th

We believe these additional allocations of capital should prove profitable in the long term as these companies embody our definition of high quality and we purchased them at attractive discounts to their long-term earnings power. They possess:

- Strong predictable cash generation

- Sustainable returns on capital, and

- Attractive growth opportunities.

Needless to say, we also revisited the balance sheets of all of our portfolio companies and went back through our stress tests on each. We also were able to finally find several attractive fixed income investments due to the massive dislocations in the bond market during the last 10 days of the quarter. As an example, we were able to buy 1-year investment grade bonds yielding 4% that a month prior yielded 1.5%. Again, please see the individual commentary on the three equity sleeves at the end of this letter for further information.

Now for some really exciting, positive news to report. I’ve been waiting for this part of the letter to elaborate on our recently announced merger with Jolley Asset Management.

I have known of Frank Jolley and his firm’s reputation for many years. I always snuck a peek at his quarterly SEC Filing 13F to see what he was buying and selling, as he and his team have an enviable long-term track record of compounding client capital. Live Oak Private Wealth was not looking for an acquisition or merger, but we heard from a close friend that Frank was looking to merge his firm with someone who offered additional muscle and expertise in comprehensive financial planning, trusts and estate work. We started exploring possibilities last August and after much consideration on both sides, we finalized the merger April 1, 2020. Jolley Asset Management brings much experience and bench strength to Live Oak Private Wealth. Frank has a talented staff including two Chartered Financial Analysts (CFA) and one Certified Public Accountant (CPA), who dovetail perfectly into our client-focused culture. Frank Jolley and his great team of Bill Collier, Terry Sapp, Jan Robillard and Stephen Bishop will remain in Rocky Mount, North Carolina and operate as a Live Oak Private Wealth business. We look forward to the day soon whereby we can get out and introduce them to you.

I feel strongly that we will get through this very disturbing time in our lives and our country’s history. It hasn’t been easy and it could continue for a while but I wouldn’t lose sight of this thought…booms plant the seeds of busts yet busts do the same in the opposite direction. The recent boom times made us all too complacent and assets expensive which allowed us to discount how good things were. It usually is in hindsight that we look back and realize how oblivious we were to hidden risks. But now we are more alert to unimaginable risks. The Federal Reserve and the government are providing massive stimulus and stocks are now priced for better future returns.

Looking back at history during very difficult times, there are many ways humans could have envisioned the world ending. But it pays to bet on humanity. Optimism during times like these never sounds “smart.” Pessimism always sounds “smarter.” But history has proven that it pays to bet big on humanity. Martin Fridson authored a book, “It Was A Very Good Year,” where he wrote that many of the best 10 years in the market in the 20th century all came after a truly horrible period like we are in.

In the future, we will have a broader imagination towards hidden threats. We are going to get through this. I believe we have many exceptional years ahead. We should feel optimistic because:

- The market will bottom

- The economy will bottom

- Humanity will prevail

- There will be better days

The other morning, I read a blog post from Morgan Housel of the Collaborative Fund that really resonated with me. When you drive by the Pentagon today, there is no trace of the plane that crashed into its walls almost 19 years ago. But drive three minutes down the road to Reagan National Airport, and the scars of September 11 are everywhere. Shoes off, jackets off, belt off, toothpaste out and empty your water bottle.

We will recover from this virus. Stores will reopen in the future. We will take a plane somewhere, stay in a hotel, go out to a restaurant and attend a Broadway play or a ballgame. The current wounds will heal just like they did after September 11. Speaking on behalf of our great team in Wilmington, Missy, Amy, Daniel, Susan, Andy and Connor, we are grateful for our health, friendship and resiliency. We are appreciative for your willingness to compensate us for doing something that is hard to do at times, but is so meaningful to us all. We remain humbled by the opportunity you have entrusted us with to protect and grow your family’s wealth.

This too shall pass.

J. William (Bill) Coleman III, CIO

and the Live Oak Private Wealth team

Focused Opportunity

Focused Opportunity Commentary and Thoughts

Our Focused Opportunity Portfolio is our signature investment portfolio which carries our highest conviction opportunities. This portfolio has unlimited flexibility to shift among styles and can appear uncomfortably idiosyncratic at times. Bargain investments can usually be found around controversial events on a company, general pessimism or those that have been performing poorly of late. Focused Opportunity invests across the capitalization spectrum and is conviction weighted to our most attractive companies.

In the first quarter, the Focused Opportunity Portfolio returned -22.24% (gross) and was down -22.24% YTD (gross).

*(See disclosure.)

Ten Largest Investments

March 31, 2020

| Year Acquired | Year Acquired | ||

|---|---|---|---|

| Berkshire Hathaway | 1998 | Disney | 2015 |

| Microsoft | 2006 | Charter Communications | 2007 |

| UnitedHealth Group | 2012 | Fed Ex | 2018 |

| Mastercard Inc | 2018 | Bank of America | 2013 |

| 2008 | CVS Health Corp | 2018 | |

During the first quarter, we bought Wells Fargo, added to Disney, Mastercard, Berkshire Hathaway and Microsoft.

Performance Attribution

| Contributors | Detractors | ||

|---|---|---|---|

| Bank of America | -40.00% | ||

| Walt Disney Co | -33.00% | ||

| Fed Ex | -20.00% | ||

| CVS Health Corp | -20.00% | ||

| Mastercard Inc | -19.00% | ||

Focused Opportunity Featured Company:

Dollar Tree (DLTR)

Dollar Tree is an operator of discount variety stores. The company operates almost 15,000 stores in 48 states and D.C. and Canada. Its segments include Dollar Tree and Family Dollar. Dollar Tree is accelerating the turnaround at Family Dollar by closing unprofitable locations, renovating others with a larger consumables assortment. We are expecting same store sales growth under the new format to grow by 10%. Dollar Tree Plus, which is being tested, offers merchandise for between $1 and $5, which could offer upside potential. The stores are highly cash generative and potential is there for Dollar Tree to earn $6 per share in 2020. This scenario supports a price of about $100 a share.

Select Portfolio

Select Portfolio Commentary and Thoughts

Our Select Portfolio might be best understood using a sports analogy. Select consists of our “bench players” or our “on deck circle” of companies. These are companies we admire and ones who compliment positions in Focused Opportunity. Select would be considered an all-cap core portfolio that is style agnostic. It invests across the capitalization spectrum yet leans towards growth. Select is also conviction weighted to companies we view have the best price to value relationship.

In the first quarter, the Select Portfolio returned -23.73% (gross) and was down -23.73% YTD (gross).

*(See disclosure.)

Ten Largest Investments

March 31, 2020

| Year Acquired | Year Acquired | ||

|---|---|---|---|

| Markel Corp | 1998 | Wal-Mart, Inc | 1998 |

| Fox Corp A | 2019 | Comcast Corp | 2004 |

| Lowes Companies | 2018 | Anthem | 2002 |

| J.P. Morgan Chase & Co | 2007 | Citigroup | 1998 |

| Cisco Systems | 1998 | Moody’s Corp | 2018 |

Portfolio Activity: During the first quarter, we added to Markel Corp.

Performance Attribution

| Contributors | Detractors | ||

|---|---|---|---|

| Citigroup | -47.00% | ||

| Fox Corp A | -36.00% | ||

| J.P. Morgan Chase & Co | -35.00% | ||

| Lowes Companies, Inc | -28.00% | ||

| Anthem | -25.00% | ||

Select Portfolio Featured Company:

Moody’s (MCO)

Moody’s Corporation is a provider of credit ratings, credit, capital markets and economic related research, data and analytical tools; software solutions and related risk management services. Moody’s, along with S&P rate more than 90% of all bonds receiving credit ratings worldwide, for a fee. Positive trends continue to favor debt issuance. Inherent in any powerful duopoly, the company possesses strong pricing power and excellent operating leverage and low reinvestment needs. Historically, Moody’s has compounded free cash flow and earnings in the low teens. Moody’s is therefore justifiably expensive at 20 times earnings, but we are comfortable with its long-term sustainable business and competitive moat.

International Portfolio

International Portfolio Commentary and Thoughts

International Portfolio: Our International Portfolio is also highly concentrated in what we feel are superior, growing businesses. The portfolio’s objective is to expose us as long-term investors to other opportunities worldwide. The mandate allows for unlimited geographical reach and can own any size capitalization business. The majority of the world’s growth is outside the U.S. and therefore, we hope to capitalize on that.

In the first quarter, the International Portfolio returned -27.85% (gross) and was down -27.85% YTD (gross).

*(See disclosure.)

Ten Largest Investments

March 31, 2020

| Year Acquired | Year Acquired | ||

|---|---|---|---|

| Nestle | 2002 | Ten Cent Holdings | 2018 |

| Alibaba | 2018 | Ferguson | 2019 |

| New Oriental Education | 2018 | Safran | 2018 |

| Unilever | 2018 | Novartis | 2018 |

| ID.Com | 2018 | Baidu, Inc | 2018 |

Portfolio Activity: During the first quarter, we bought Exor.

Performance Attribution

| Contributors | Detractors | ||

|---|---|---|---|

| JD.Com | +15.00% | Unilever | -15.00% |

| Ten Cent Holdings | +2.00% | Novartis | -13.00% |

| New Oriental Education | -11.00% | ||

| Alibaba | -8.00% | ||

| Nestle | -5.00% | ||

International Portfolio Featured Company:

Exor (EXXRF)

Exor is an Italian holding company for the Agnelli family which holds Fiat, Ferrari, CNH Industrial and soon to be disposed PartnerRe. The investment case for Exor is the capital allocation acumen of John Elkann, the grandson of Gianni Agnelli. His track record of meaningfully compounding business value over time coupled with the incoming proceeds ($9B) of PartnerRe constitutes a golden opportunity in our opinion. There is currently a misperception in the market as to the value of Exor, due to the many complexities and layers of ownership in the corporation. Exor will evolve tremendously over time as it intelligently deploys the proceeds from the sale of PartnerRe. Exor could possibly be valued currently at a 50% discount to its NAV or its sum of the parts.

Appendix

Live Oak Private Wealth Investment Philosophy

Three Pillars

We consider potential losses before gains. We think about multiple scenarios that could affect us. We ask how much we might lose before we ask how much we might make.

We focus on absolute returns, not relative returns. Our goal is to lose less than the market. We don’t manage to a benchmark.

We do not focus on the macroeconomic environment. We focus on truly great businesses we can invest in at a fair price.

Our Beliefs

We believe your lifetime investment results will be mostly governed by two variables: behavior and asset allocation.

We consider the three quotes below by two very famous investors daily in our thoughts, research and work.

“To buy when others are despondently selling and to sell when others are avidly buying, requires the greatest

fortitude and pays the greatest reward.”

John Templeton

“Be fearful when others are greedy and greedy when others are fearful.”

Warren Buffett

“Price is what you pay, value is what you get.”

Warren Buffett

Guiding Principles

- A share of stock represents a share in the ownership of a business.

- A stock exchange is nothing more than an auction place that provides a convenient means for exchanging your ownership in a business for cash and vice-versa.

- Our investment approach would be akin to applying a private equity mindset to investing in public markets.

- We limit our search for qualifying investments to good businesses. They have identifiable, sustainable competitive advantages.

- Risks to us is permanently losing capital over a five-year time horizon. Market volatility is not risk to us.

- Our primary return goal is to compound capital at real rates of return (4-5%) in excess of inflation over our five-year time horizon.

- Compounding capital at 7% doubles your assets in 10 years.

Disclosures

1) Past performance is no guarantee of future results and future performance may be higher or lower than the performance shown. The performance results for each equity sleeve are calculated for us by Orion Services and does not reflect investment management fees, custody and other costs or taxes. All of which would be incurred by an investor in any account managed by Live Oak Private Wealth.

2) The performance results for each equity sleeve assumes a full and static investment in the respective sleeve for the periods stated, whereas an account managed by Live Oak Private Wealth may not have a full and static investment in each position and may hold a cash position. A client’s actual net performance of their account would most likely be different and generally would be lower.

3) The performance results for each equity sleeve does not and is not intended to indicate past or future performance for any account or investment strategy managed by Live Oak Private Wealth.

4) There can be no assurance that our portfolio management or any account managed by our investment managers will achieve a targeted rate of return or volatility or any other specified parameters. There is no guarantee against loss resulting from an investment.

5) Investment objectives, returns, and volatility are used for measurements and/or comparison purposes only and are only a guideline for prospective investors to evaluate our investment strategy and the accompanying risk/reward ratios.

6) Comparison to any index is for illustrative purposes only. Certain information, including index and benchmark information, has been provided by third-party sources, and although believed to be reliable, has not been independently verified and its accuracy cannot be guaranteed.

7) The information contained here is not complete, may change, and is subject to, and is qualified in its entirety by, the more complete disclosures, risk factors, and other important information contained in Part 2A or 2B of Form ADV. This presentation is for informational purposes only and does not constitute an offer to sell or as a solicitation.

8) Live Oak Private Wealth is a subsidiary of Live Oak Bank. Investment advisory services are offered through LOPW, LLC, an Independent Registered Investment Advisor.

9) Opinion and thoughts expressed are those of Bill Coleman and not Live Oak Bank.

Download the final letter of 2019 to learn more about Live Oak Private Wealth’s portfolio activity, performance characteristics and comments from the team.

Introduction

“The reasonable man adapts himself to the world, the unreasonable one persists in trying to adapt the world to himself. Therefore all progress depends on the unreasonable man.”

– George Bernard Shaw

What a difference a year can make. I would have never imagined this time last year that 2019 would have produced the best stock returns since 2013. The market as measured by the S&P 500 missed having the best year since 1997 by a mere 20 points or less than 1%. 2019 couldn’t have looked any more different than 2018. In 2018, every asset class closed down on the year, except cash.

Stocks around the world closed out one of the best years of the past decade, defying all of the pundits (including me) who began the year expecting the late-stage economy and roaring bull market to be upended by all of the worries we ended last year with. The backdrop was all doom and gloom, as the global economy seemingly was weakening, the Federal Reserve was tightening monetary policy and that in turn would accelerate the slowdown turning the market towards a protracted downturn, versus just a two-month correction.

Now, we close out the year with stock indexes from the U.S. to Europe to Brazil up more than 20%. Considering the decade we just finished, the Wall Street Journal calculates the Dow Jones Industrial average’s return was 170% from 2010-2019. This was the fourth best decade in the last 100 years. According to Howard Silverblatt of Standard and Poors, the S&P 500 Index returned over 250% over the decade. S&P data from the time they started tracking it in the 1930’s, showed the best decade on record was the 1950’s when the market produced 19% average annual returns. It wasn’t too long ago that we remember the worst decade of stock performance, the 2000’s (2000-2009). Stocks remarkedly fell almost 1% compounded annually, as the decade was bookended by the dot.com tech bubble crash in 2000-2001 and then the financial crisis in 2008.

Considering the fact that I’m finishing my third full decade (1990’s, 2000’s and 2010’s) in the investment business, it’s quite enlightening to see the variation of returns over 10-year periods. But never in my 34-year career would I have ever imagined that, conceptually, “money is free” for creditworthy investors. Fixed income investors are accepting negative or very, very low interest rates and don’t require having their principal paid back for the foreseeable future. There are over $15 trillion of government bonds worldwide that now trade at negative yields because central banks are buying up financial assets in a futile attempt to produce growth in GDP and other economic activity and get inflation up.

The ultra-low yields globally are sending signals we haven’t seen before. Many interpret these signals as proposing that yields are now more affected by sustained demand for long-term government bonds, in part because of demographics and an aging society and deficits. One thing for sure, I think …. is that the ultra-low and negative rates have fueled extra demand for equities. Interest rates are a key input in quantitative, passive “factor” investing strategies who (a machine) picks stocks based on categories such as growth, momentum, quality or value. This year saw another liquidity fueled flow of funds into the growth factor arena. The ultra-low rates have been the rocket fuel for the momentum behind the move up in growth stocks, especially technology (more on this later).

2019 was a very good year for Live Oak Private Wealth, the business. We were privileged to have many new clients join our firm and for the benefit of them especially, I always try and revisit our investment philosophy and write a little about our process in these letters for new readers. Please also see our appendix for additional details about our core beliefs and process.

Our investment philosophy is deeply rooted in a strongly held conservative belief in being very careful with money. We understand the mathematics of compounding and therefore concentrate our decision making around avoiding losses as much as possible. We do that from continued learning and experience we have gained from the study of the world’s most accomplished investors, such as Benjamin Graham and Warren Buffett. Graham’s key insight and the basis of Buffett’s success is that investing is successful when it’s businesslike. We don’t focus on “stocks, bonds or markets”…we look at the businesses these securities represent. Businesslike investing has another important distinction. Most traders and market participants seldom recognize, and typically ignore, the fundamental distinction between price and value. We seek to buy businesses whose value exceeds their price. When we have found suitable securities, we combine them into portfolios. Since there are always factors outside of our control, we try to manage these with some degree of diversification. But, we want to concentrate our capital in a relatively small number of what we believe to be growing and competitively advantaged businesses. These kinds of businesses are rare and are only periodically available for purchase at attractive valuations. With this in mind, we do our best to hold these businesses for the long term, so that our capital may compound as the business grows.

Since our wheelhouse is the public securities market in most part, we deal daily with “the market.” We view the public market or exchanges as what they really are….auctions, where money is exchanged for pieces of a business. You don’t go to an auction every day and you certainly shouldn’t go there if the price of whatever you are considering exchanging cash for isn’t to your advantage. The public spends much time talking about “the market.” The media (social, print and cable), spews chatter, noise and hype about it daily. All of this stuff about the market is unknowable. Is the market going up or down? What about the impeachment? What about an inverted yield curve? This is the longest bull market in history….yadda, yadda. This is where the distinction between speculation and businesslike investing comes from. Investing, is the craft of the specific and legendary investor John Train, even wrote a book about this titled The Craft of Investing. Therefore, specifically at times, without regards to the level of a market, there can be very good specific intelligent investments to make. We see several presently, even with the U.S. market at an all-time high.

Much of the current market phenomenon centers around the more expensive growth stocks increasing in value while many of the least expensive stocks remain relatively cheaper and more reasonably attractive. As we sit currently, the U.S. market is at an all-time high, yet fewer stocks are contributing to the rally. You may hear about “styles” of stocks that are categorized as either growth or value, and growth stocks outpacing (outperforming) value stocks. We don’t spend too much time worrying about style boxes such as these, as we spend much time identifying, researching and hopefully buying extraordinary businesses run by exceptional people with abundant reinvestment opportunities. We look for these great businesses to have copious amounts of excess cash at the end of each year and intelligent uses for that cash for reinvestment. Imagine the concept of “earning money on top of earnings.” This is the compounding we speak to. This is how patient investors over the years in companies such as Walmart, TJ Maxx, Southwest Airlines, Starbucks, etc., have made vast fortunes in businesses like these. They continued to compound due to the many opportunities to invest the excess cash flow each year. Many of our portfolio companies have experienced much success as well as holdings such as United Healthcare, CarMax, Apple, Charter Communications and Google have compounded at rates in excess of the public markets.

An experienced and talented money manager I know in Rocky Mount, N.C. asked me recently what I thought of “the market.” I replied that it felt a lot like the late 1990s where momentum was very strong. The period from 1997 to 2000 saw growth style stocks outperform value style stocks, like today. There was concentration in a few big tech stocks that powered the indexes, like today. The important distinction between now and then is that the total market is not priced at excessive and dangerous levels as it was in 1999-2000. But, there are some similar dangerous undercurrents we are watching. Consider these statistics: As of September 30, 2019, six businesses – Facebook, Amazon, Netflix, Microsoft, Apple and Google (FANMAG) had a combined capitalization of $4.3 Trillion, representing nearly 14% of the total U.S. market capitalization (according to Research Affiliates). If these six stocks were viewed as a single nation, the country of “FANMAG” would be more valuable than the entire publicly traded markets of the United Kingdom, China, France or Germany. If we were to remove these six stocks from the market’s technology sector, we would be left with a sector now “smaller” than either the financial or healthcare sectors. Apple and Microsoft (which we own) combined are worth more than the entire Russell 2000 Index.

We worry that these most dominant companies, 7 of the 10 largest global companies by market cap, all come from just one sector of the market, technology. Interestingly, at the top of the dot.com bubble in 2000, the technology sector was less dominant than it is today. The top technology stocks from 2000 underperformed the S&P 500 over the next decade and two companies disappeared entirely. Many of you probably don’t remember a company called Palm. They made the PalmPilot (I had one) which was disrupted out of business by Blackberry who was disrupted out of business by Apple’s iPhone. Palm was once more valuable than General Motors. The Live Oak Private Wealth Investment Team is watching the valuations of our large tech stocks very carefully.

Portfolio(s) Discussion and Commentary

Our investment team manages three equity portfolios in addition to our fixed income solutions. Each of these three equity portfolios are unique with different approaches. Please see individual commentary on each at the end of this letter.

As the markets rose materially in the fourth quarter, many companies met or exceeded our valuation metrics. We have fairly stringent screens for companies to pass through to remain relevant in our portfolio sleeves. Given the level of the markets and where we feel we are in the economic cycle, as well as the geo-political risks that are still with us….we have combined two of our investment sleeves into one. Equity Income and Select are now one sleeve. Several businesses in these two sleeves were not making it through our price to value filter and from a risk management perspective, we opted to consolidate the 50 or so positions down to 25 by positioning “new” Select in our best risk adjusted businesses. Additionally, we don’t want to dilute our research time and efforts by not having the ample resources for our best ideas.

The Live Oak team has been busy during the fourth quarter with other analysis as well. We participated in three “Investor Days” with United Healthcare, Liberty Media and Brookfield Asset Management. After hearing from all levels of management with these companies as well as getting updates and prospects for 2020, we remain very comfortable with these investments.

So we now find ourselves at the dawn of a new year and new decade. Lots of considerations, risks and rewards to contemplate. We had a phenomenal year in 2019. Most all of us find ourselves at a high-water mark with our investment account values. Now is the time to revisit your comprehensive financial plan and asset allocation. It could be an opportune time to rebalance and gain a better position for what may lie ahead. Don’t hesitate to reach out to any one of the Live Oak Private Wealth team to schedule a comprehensive financial planning review.

So, what may lie ahead? I have a long list of worries and considerations that our team will be monitoring as we go through the year:

- A very important political election.

- Potential effects of tightening liquidity conditions against a backdrop of ever-increasing corporate debt levels.

- Potential for the economics of the past to result in some wage inflation given the strong U.S. consumer and low levels of unemployment.

- Continued struggles of “unicorns” accessing the public markets via I.P.O.’s. Private Equity deal making, and venture capital speculation is rampant, fueled by continued low interest rates.

- Excessive optimism. Most all sources of measuring investors’ sentiment are showing extreme optimism (highest in 15 years).

- Continued cold war of trade globally between the U.S. and China and Brexit with the European Union.

- My long-standing worry about the markets structure and the risks inherent in quantitative factor investing driven by computers and fueled by the sheer size of ETF’s.

I could go on, but I’ll stop. I will remind you though that our job is to do the worrying for you and to make as many intelligent investment decisions for you as we can without having a crystal ball. Our job too is to educate you about what we are doing and why. We strive to remind you that one of the most important things you can do to help your chances of success is to take a long-term view. Many times, investors fail to earn the rate of returns the markets produce due to investors letting their emotions (fears) get the best of them and cause them to sell at inopportune times or chase a fad too long.

To continue to be successful creating wealth in the public markets, you have to take a multi-year view. Consider these facts, courtesy of J.P. Morgan…since 1950, the range of stock market returns as measured by the S&P 500 in any given year has been from +47% to -37%. But over any 5-year period the range is +28% to -3%. For any given 20-year period, the range of outcomes contracts still further to +17% to +6%. In short, since 1950, based on J.P. Morgan data, there has never been a 20-year period when investors did not earn at least 6% in the market. Obviously, history can sometimes not repeat, and this historical data is by no means a guarantee of the future, but history has shown that keeping a long-term time horizon pays off.

In conclusion, we had a fantastic year! I want to thank you for your steadfast support of Live Oak Private Wealth. We have worked tirelessly to assemble what we feel is the best team of people, offerings of investment strategies and financial wealth planning. I read several books this quarter but Excellence Wins by Horst Schulze, co-founder of the Ritz Carlton hotel company resonates well where I view Live Oak Private Wealth as we end the year and decade. Horst Schulze’s vision for the Ritz Carlton was to strive for the exceptional. He had a vision and he crafted people-focused standards that made the Ritz into what it is. We are trying to create a culture of service modeled after his vision. Under Schulze’s leadership, the company committed to the highest standards of professionalism and created systems to achieve them. Our team at Live Oak Private Wealth has made great strides this year refining and executing on our vision of the “best of the best” in the wealth management industry. Our team implemented new systems during the fourth quarter to leverage our service commitment to you. Therefore, our experienced people, skills and innovation is our competitive advantage and we will continue to strive for excellence in all aspects of our relationship.

Thank you for allowing us to innovate and strive to get better every day. We are fortunate to have resources for investment in systems and professional development to get even better serving you. We are grateful and appreciative for your willingness to compensate us for doing something that we love to do and is so meaningful to us all. We are humbled by the opportunity you have given us to protect and grow your family’s wealth.

Speaking on behalf of our great team … Missy, Amy, Daniel, Susan, Andy and Connor, we look forward to our continued shared success in this partnership.

With warmest regards,

J. William (Bill) Coleman III

and the Live Oak Private Wealth Team

Focused Opportunity

Focused Opportunity Commentary and Thoughts

Our Focused Opportunity Portfolio is our signature investment portfolio which carries our highest conviction opportunities. This portfolio has unlimited flexibility to shift among styles and can appear uncomfortably idiosyncratic at times. Bargain investments can usually be found around controversial events on a company, general pessimism or those that have been performing poorly of late. Focused Opportunity invests across the capitalization spectrum and is conviction weighted to our most attractive companies.

In the fourth quarter, the Focused Opportunity Portfolio returned 10.13% (gross) and was up 32% YTD (gross).

*(See disclosure.)

Ten Largest Investments

December 31, 2019

| Year Acquired | Year Acquired | ||

|---|---|---|---|

| Berkshire Hathaway | 1998 | United Healthcare | 2012 |

| Apple | 2011 | CarMax | 2018 |

| Microsoft | 2006 | Charter Communications | 2007 |

| Bank of America | 2013 | CVS Health Corp | 2018 |

| 2008 | Abbot Labs | 2016 | |

Portfolio Activity: During the fourth quarter, we conducted a tax swap with FedEx and made additions to Dollar Tree.

Performance Attribution

| Contributors | Detractors | ||

|---|---|---|---|

| United Health Group | +35.00% | Dollar Tree | -17.00% |

| Apple | +31.00% | CarMax | -1.00% |

| HCA Healthcare | +26.00% | ||

| Charles Schwab | +26.00% | ||

| Bank of America | +24.00% | ||

Focused Opportunity Featured Company:

United Health Group (UNH)

United Health Group is the nation’s largest publicly traded managed care company. It operates through two business segments, United Healthcare and Optum. United Health is a diversified healthcare company dedicated to helping people live healthier lives and helping make the health system work better for everyone. From an investor’s standpoint, UNH boasts best in class health costs per member, allowing it to price its insurance offerings more attractively to drive above-peer enrollment growth. Their strategy of pursuing scale across multiple healthcare services verticals creates inherent synergies that solidify its competitive position. Strong continued trends should result in $16-$17 per share in earnings in 2020 continuing the trend of solid earnings growth.

Select Portfolio

Select Portfolio Commentary and Thoughts

Our Select Portfolio might be best understood using a sports analogy. Select consists of our “bench players” or our “on deck

circle” of companies. These are companies we admire and ones who compliment positions in Focused Opportunity. Select

would be considered an all-cap core portfolio that is style agnostic. It invests across the capitalization spectrum yet leans

towards growth. Select is also conviction weighted to companies we view have the best price to value relationship.

In the fourth quarter, the Select Portfolio returned 6.99% (gross) and was up 29.04% YTD (gross).

*(See disclosure.)

Ten Largest Investments

December 31, 2019

| Year Acquired | Year Acquired | ||

|---|---|---|---|

| Google A | 2009 | Comcast | 2004 |

| Fox Corp A | 2019 | Anthem | 2002 |

| Citigroup | 1998 | 2019 | |

| Lowes Companies | 2018 | Mohawk Industries | 2018 |

| Markel | 1998 | J.P. Morgan | 2009 |

Portfolio Activity: During the fourth quarter, we performed a deep dive into the appraisals of price to value on all Select and

Equity Income positions and consolidated the two sleeves into what we now consider the best of the best.

Performance Attribution

| Contributors | Detractors | ||

|---|---|---|---|

| Anthem | +27.00% | Boeing | -13.00% |

| Target | +21.00% | Restaurant Brands | -10.00% |

| Liberty Sirius XM | +18.00% | American International Group | -6.00% |

| Citigroup | +17.00% | Cheniere Energy | -3.00% |

| +17.00% | Markel | -2.00% | |

Focused Opportunity Featured Company:

Markel (MKL)

Markel is a financial holding company based in Richmond, Virginia and was formed in 1930 to sell insurance to taxicabs and buses. Today the company underwrites specialty insurance products in a variety of markets around the world. Markel possesses an outstanding investment track record, similar to Berkshire Hathaway. Management, culture, investing acumen and flexibility are all hallmarks of Markel. Markel has compounded book value at 20% since 1980 versus 10% for the S&P 500. Its stock price has compounded at 17% since going pubic 27 years ago. Currently we find its stock price to book value relationship quite attractive.

International Portfolio

International Portfolio Commentary and Thoughts

International Portfolio: Our International portfolio is also highly concentrated in what we feel are superior, growing businesses. The portfolio’s objective is to expose us as long-term investors to other opportunities worldwide. The mandate allows for unlimited geographical reach and can own any size capitalization business. The majority of the world’s growth is outside the U.S. and therefore, we hope to capitalize on that.

In the fourth quarter, the International Portfolio returned 12.75% (gross) and was up 29.29% YTD (gross).

*(See disclosure.)

Ten Largest Investments

September 30, 2019

| Year Acquired | Year Acquired | ||

|---|---|---|---|

| Nestle | 2002 | Vivendi | 2019 |

| Alibaba | 2018 | Safran | 2018 |

| New Oriental Education | 2018 | JD.Com | 2018 |

| Fiat Chrysler | 2018 | Ten Cent Holdings | 2018 |

| Ferguson | 2019 | Airbus Group | 2018 |

Portfolio Activity: During the fourth quarter, we initiated a new position: Vivendi and sold Prosus which was spun off from Naspers.

Performance Attribution

| Contributors | Detractors | ||

|---|---|---|---|

| Alibaba | +28.00% | Safran | -2.00% |

| JD.Com | +25.00% | ||

| Baidu | +24.00% | ||

| Ferguson | +22.00% | ||

| Fiat Chrysler | +15.00% | ||

Focused Opportunity Featured Company:

Vivendi (VIVHY)

Vivendi is a French conglomerate whose major asset is Universal Music Group. UMG is the largest music label in the world and drives the majority of the earnings of the company and represents the majority of Vivendi’s value. Our thesis behind the purchase of Vivendi is somewhat of a sum of the parts story as well as a play on the growth of music streaming. UMG is the major player in the streaming music industry supplying most of the music to the likes of Spotify, Pandora and Apple Music. Growth is robust and Vivendi is monetizing a small piece of UMG and will be buying back shares with the proceeds. We estimate Vivendi is undervalued by 30% or more.

Appendix 1

Live Oak Private Wealth Investment Philosophy

Three Pillars

We consider potential losses before gains. We think about multiple scenarios that could affect us. We ask how much we might lose before we ask how much we might make.

We focus on absolute returns, not relative returns. Our goal is to lose less than the market. We don’t manage to a benchmark.

We do not focus on the macroeconomic environment. We focus on truly great businesses we can invest in at a fair price.

Our Beliefs

We believe your lifetime investment results will be mostly governed by two variables: behavior and asset allocation.

We consider the three quotes below by two very famous investors daily in our thoughts, research and work.

“To buy when others are despondently selling and to sell when others are avidly buying, requires the greatest

fortitude and pays the greatest reward.”

John Templeton

“Be fearful when others are greedy and greedy when others are fearful.”

Warren Buffett

“Price is what you pay, value is what you get.”

Warren Buffett

Guiding Principles

- A share of stock represents a share in the ownership of a business.

- A stock exchange is nothing more than an auction place that provides a convenient means for exchanging your ownership in a business for cash and vice-versa.

- Our investment approach would be akin to applying a private equity mindset to investing in public markets.

- We limit our search for qualifying investments to good businesses. They have identifiable, sustainable competitive advantages.

- Risks to us is permanently losing capital over a five-year time horizon. Market volatility is not risk to us.

- Our primary return goal is to compound capital at real rates of return (4-5%) in excess of inflation over our five-year time horizon.

- Compounding capital at 7% doubles your assets in 10 years.

Disclosures

1) Past performance is no guarantee of future results and future performance may be higher or lower than the performance shown. The performance results for each equity sleeve are calculated for us by Orion Services and does not reflect investment management fees, custody and other costs or taxes. All of which would be incurred by an investor in any account managed by Live Oak Private Wealth.

2) The performance results for each equity sleeve assumes a full and static investment in the respective sleeve for the periods stated, whereas an account managed by Live Oak Private Wealth may not have a full and static investment in each position and may hold a cash position. A client’s actual net performance of their account would most likely be different and generally would be lower.

3) The performance results for each equity sleeve does not and is not intended to indicate past or future performance for any account or investment strategy managed by Live Oak Private Wealth.

4) There can be no assurance that our portfolio management or any account managed by our investment managers will achieve a targeted rate of return or volatility or any other specified parameters. There is no guarantee against loss resulting from an investment.

5) Investment objectives, returns, and volatility are used for measurements and/or comparison purposes only and are only a guideline for prospective investors to evaluate our investment strategy and the accompanying risk/reward ratios.

6) Comparison to any index is for illustrative purposes only. Certain information, including index and benchmark information, has been provided by third-party sources, and although believed to be reliable, has not been independently verified and its accuracy cannot be guaranteed.

7) The information contained here is not complete, may change, and is subject to, and is qualified in its entirety by, the more complete disclosures, risk factors, and other important information contained in Part 2A or 2B of Form ADV. This presentation is for informational purposes only and does not constitute an offer to sell or as a solicitation.

8) Live Oak Private Wealth is a subsidiary of Live Oak Bank. Investment advisory services are offered through LOPW, LLC, an Independent Registered Investment Advisor.

9) Opinion and thoughts expressed are those of Bill Coleman and not Live Oak Bank.

Download the full third quarter 2019 letter to learn more about Live Oak Private Wealth’s portfolio activity, performance characteristics and comments from the team.

“Basically, price fluctuations have only one significant meaning for the true investor. They provide them with an opportunity to buy wisely when prices fall sharply, and to sell wisely when they advance a great deal. At other times, he will do better if he forgets about the stock market and pays attention to his dividend returns and to the operating results of his companies.”

– Benjamin Graham, Columbia University professor

Introduction

Before we get into the investment thoughts and highlights from the third quarter, Live Oak Private Wealth is excited to report that we have launched corporate trustee services led by our skilled fiduciary professional, Daniel Hughes. This local, personalized service dovetails perfectly into our existing trust and estate services, which help protect personal wealth today and for generations to come. Make sure to visit our website to read Daniel’s recent blog post about our trust offering as well as other important content from the team regarding goal-based financial planning, retirement cash flow planning, investment tax considerations and charitable giving.

We all know time flies, especially as we age, but it is hard to believe that Live Oak Private Wealth is a year old! What a first year we have had. We are all excited with what we have built thus far and where we are going with our team’s collective vision of wealth management. If any of you are reading this and haven’t yet met our entire team and seen our beautiful campus, please do so. We have a compelling story to share with you.

The U.S. market, as measured by the S&P 500, managed to squeeze out a slight increase in the third quarter. By doing this, the U.S. market held on to its largest year-to-date gains in recent memory. This has continued to prolong one of the longest bull markets in history. Bonds rose as well and declining interest rates have helped drive stock market returns upward, while at the same time reflecting the uncertainty investors feel about the global economy, trade wars with China and the Fed’s decisions around easing or tightening. The U.S. economy, as measured by the consumer, remains on strong footing, yet there are concerns that the longer the trade war with China rolls on, the higher the probability that the U.S. consumer will start to feel the negative effects and become more cautious.

While the quarter ended quietly, it was loud and volatile underneath the surface. Stocks ramped up to new highs in July but then dropped hard in August only to claw its way back up to a slight gain in September. Every quarter that goes by, it seems that there is more and more uncertainty, volatility and unease. Most of this directly relates to geopolitics and especially Washington. When I think about it, never in my 33-year investment career have I seen so much seemingly revolving around what will happen from a political perspective. There is massive polarity when contemplating the agendas of the two parties. When studying past market and presidential election cycles, typically if the U.S. economy is doing well and unemployment is low, inflation is in check, the incumbent president is usually re-elected. This next election will be more than interesting.

U.S. politics, elections and other global geopolitics tend to move markets more now than ever in history. This is most likely due to the significant change in the public stock market structure now that passive assets outweigh active assets and algorithmic computerized trading of exchange traded funds is leading to increased volatility. You, as a reader of these letters, may be as tired of reading about the risks we see related to the computerized trading as we are about writing about them. But the influence of “rules based” computerized trading strategies, that key off interest rates, geopolitics, trade and tweets, continues to grow more extreme by the quarter. According to J.P. Morgan, passive strategies now control 60% of U.S. equity trading volume while quantitative funds control another 20%, a staggering 80% combined. And based on a recent report by Thomson Reuters, algorithmic trading systems are now responsible for 75% of global trading volumes. None of these strategies have been tested in a recession. Exchange traded funds, especially the dominant capitalization weighted ones, have not been tested to see if the “daily liquidity” that the “machines” thrive on, pairs well with the far less than daily liquidity of the assets underlying the ETFs. It’s unclear and unnerving to us whether modern market makers will provide the liquidity necessary to

stabilize markets in the event of a crisis.

One of the core tenants of Live Oak Private Wealth’s investment philosophy is understanding and recognizing that in investing, you win more by losing less. Many investors today pay more attention to returns than risks, while our approach argues for the opposite: Pay more attention to risks than returns. Risk is omnipresent, and managing it is about assessing the variations of risk such as computerized trading or excessive valuation of recent “unicorns” that have come public. Some form of risk is inherent in all aspects of long-term investing and the key to mitigating it is being aware and conscious of it daily.

Now that we are ten years into this bull market cycle since the financial crisis, thankfully most all investors are enjoying a high-water mark of wealth. Most investment accounts are fairly flush, and the balances are large. We focus on that because you always lose money downward from a bigger number and gain money upward from a lower number. Remember this example: if your investment portfolio is worth $1,000,000 and you expose it to a 50% loss, it becomes $500,000. Then you need for your $500,000 portfolio to double (go up by 100%) simply to break even. It is very tough to find stocks or markets with 100% upside. It can take years to get back to break even. On the other hand, if you can keep your portfolio exposed to say a 20% decline or $800,000, your opportunity to recover is easier and shouldn’t take as long. If you are in retirement or getting close to retirement, this mathematical principal is very important to your financial longevity. We get it.

Having now recovered, enlightened and informed by my travels to Italy and Croatia this summer, I was surprised by the level of global tourism I witnessed. It had been a while since I was last in Europe, and it was eye opening to see the number of global travelers, especially in that region of the world. It was so exciting to see firsthand what we hear about in regard to a growing middle class in the world. All I could think about was one of our research theses around global transportation. It was hard for me to appreciate the statistic below, yet I experienced it for myself by the sheer numbers of global travelers I saw from all over the world.

| United States as a percent of the world’s population | 5% |

| United States as a percent of the world’s GDP | 25% |

It is hard to comprehend the effects of a growing global middle class, especially travel and tourism. Based on statistics by the United Nations and the OECD, the global middle-class population was 1.8 billion in 2009 and is estimated to be 3.2 billion next year and 4.9 billion in 2030. Middle class spending is increasing and shifting from the U.S. to the rest of the world. Again, using estimates from the OECD, consider these statistics:

| 2009 Middle class spending | $21 trillion | 26% U.S. | 74% rest of the world |

| 2020 Middle class spending (est.) | $35 trillion | 17% U.S. | 83% rest of the world |

| 2030 Middle class spending (est.) | $55 trillion | 10% U.S. | 90% rest of the world |

Considering our investment thesis around global transportation, the world’s transportation infrastructure has not kept pace with the rising demand for travel by this massive growing percentage of middle-class individuals globally, therefore we have investments in French airplane manufacturer Airbus Industries and airplane engine maker Safran. Given that some statistics show miles flown growing at 6% a year, we can see hopefully a long-term trend benefitting us.

One of the many core competencies of the Live Oak Private Wealth team is knowing as much as possible about our businesses we are invested in. Our research effort casts a wide net. This quarter, we traveled to New York in September to attend two investment conferences, both of which also eluded to the many global investment opportunities. We split our time over the two days trying to gather as much research and understanding as possible. I attended a conference put on by MOI Global called Latticework, which has been lauded as a uniquely impactive interactive forum of the best minds from the MOI Global community. There were many takeaways, but a presentation by Rupal Bhansali from Ariel Investments was particularly insightful and led me to read her recent book, “Non-Consensus Investing.” Connor was in different meetings with other contacts and trying to connect with a prominent money manager who was attending Mastercard’s (another core portfolio holding) analyst day at the New York Stock Exchange. The next day we both tag-teamed a day of research with the global investment team at Davis Advisors. We came home that night with strong convictions around several businesses we are invested in, such as New Oriental Education, United Technologies, Alibaba and financials such as Bank of America. We are fortunate to have such a well-rounded and diversified team at Live Oak Private Wealth and to be able to travel to these types of conferences to learn from those smarter than us and benefit from variant perceptions that you gain by getting away from your daily, biased, home-research routine.

So, as we look out to the fourth quarter, 2020 and beyond, we remain confident in the long-term fundamental strength of the American economy, yet in the next 14-15 months we will undoubtedly experience politically based volatility unlike anything seen in more than a generation. This volatility will occasionally feel quite uncomfortable and we will be working overtime to try and separate real risk from perceived risk during these uncertain times. We will be trying to 1) figure out what we know, 2) figure out what we don’t know and 3) figure out what we can’t know. We will remain diligent towards risk management at the possible expense of returns. We are keenly aware of the fact that much of your savings you are entrusting us with is irreplaceable. We understand that survival is the key to investment success and to finish first, you must finish. Above all else, we will maintain our steady course of intelligent, long-term investing…always looking for quality businesses that are undervalued or misunderstood to opportunistically capitalize on with our shared capital.

Our team reads many quarterly letters such as this one from many other smart, successful investment teams. We were reading one from Don Yacktman where he referenced “Hakuna Matata,” which translates as “no worries,” and is a popular song from “The Lion King,” the Disney blockbuster movie and Broadway show. The philosophy of “no worries” has prevailed for quite a while during the last ten years and the market returns pan that out. We believe when people are not worried, you should worry. “Hakuna Matata” didn’t work out well in “The Lion King” and is not an intelligent investment approach by our standards. We believe it is important for you to have a team of advisors and investment professionals like us who will worry for you. We have experienced volatile environments and risks before, and we will navigate through them in the future by focusing on our disciplined investment strategy. We will remain vigilant toward the risks that are inherent today.

We remain humbled and appreciative by your willingness to compensate us for doing something that we love to do and is so meaningful and rewarding to us all. Our entire Live Oak Private Wealth team looks forward to our continued shared success in this partnership.

With warmest regards,

J. William (Bill) Coleman III

and the Live Oak Private Wealth Team

Portfolio(s) Discussion and Commentary

Our investment team manages four equity portfolios in addition to our fixed income solutions. Each of these four equity

portfolios are unique with different approaches.

Focused Opportunity

Focused Opportunity Commentary and Thoughts

Our Focused Opportunity Portfolio is our signature investment portfolio which carries our highest conviction opportunities. This portfolio has unlimited flexibility to shift among styles and can appear uncomfortably idiosyncratic at times. Bargain investments can usually be found around controversial events on a company, general pessimism or those that have been performing poorly of late. Focused Opportunity invests across the capitalization spectrum and is conviction weighted to our most attractive companies.

In the third quarter, the Focused Opportunity Portfolio returned 2.08% (gross) and is up 19.31% YTD (gross).

Ten Largest Investments

September 30, 2019

| Year Acquired | Year Acquired | ||

|---|---|---|---|

| Berkshire Hathaway | 1998 | United Healthcare | 2012 |

| Apple | 2011 | CarMax | 2018 |

| Microsoft | 2006 | Charter Communications | 2007 |

| Bank of America | 2013 | CVS Health Corp | 2018 |

| 2008 | Abbot Labs | 2016 | |

Portfolio Activity: During the third quarter, we sold Bank of New York and made small additions to Charles Schwab and Fed Ex.

Performance Attribution

| Contributors | Detractors | ||

|---|---|---|---|

| CVS Health | +14.82% | Schlumberger | -13.10% |

| Apple | +11.12% | Fed Ex | -10.68% |

| +11.03% | HCA Healthcare | -10.50% | |

| Brookfield Asset Mgmt. | +10.10% | United Healthcare | -10.44% |

| Verizon Communications | +6.53% | Walt Disney | -8.00% |

Focused Opportunity Featured Company:

Berkshire Hathaway

Berkshire is currently trading at one of the widest discounts to intrinsic value in many years. Being a conglomerate, Berkshire is one of the least followed and misunderstood large cap companies in the market. Berkshire’s value is derived by almost half insurance and half in diversified operating companies such as MidAmerican Energy, Burlington Northern Railroad, Clayton Homes, Shaw Carpet, Benjamin Moore and others. Many, including us, value Berkshire at a multiple of 14 times earnings, which we feel are understated in the current low interest rate environment. Given Berkshire’s cash hoard of over $100 billion, we expect a sizable accretive acquisition during the next downturn. Berkshire has also adjusted its buyback policy which should continue to enhance our returns.

Select Portfolio

Select Portfolio Commentary and Thoughts

Our Select Portfolio might be best understood using a sports analogy. Select consists of our “bench players” or our “on deck circle” of companies. These are companies we admire and ones who compliment positions in Focused Opportunity. Select would be considered an all-cap core portfolio that is style agnostic. It invests across the capitalization spectrum yet leans towards growth. Select is also conviction weighted to companies we view have the best price to value relationship.

In the third quarter, the Select Portfolio returned 1.24% (gross) and is up 20.28% YTD (gross).

Ten Largest Investments

September 30, 2019

| Year Acquired | Year Acquired | ||

|---|---|---|---|

| Google A | 2009 | Comcast | 2004 |

| Fox Corp A | 2019 | Anthem | 2002 |

| Citigroup | 1998 | 2019 | |

| Lowes Companies | 2018 | Mohawk Industries | 2018 |

| Markel | 1998 | Liberty Sirius XM | 2007 |

Portfolio Activity: During the third quarter, we made no portfolio changes.

Performance Attribution

| Contributors | Detractors | ||

|---|---|---|---|

| Lennar Corp. | +16.16% | Mohawk | -17.68% |

| Medtronic PLC | +10.72% | Anthem | -15.08% |

| Liberty Sirius XM | +8.96% | Apache | -12.33% |

| Lowes | +7.59% | Fox Corp A | -12.21% |

| Markel | +7.01% | Cheniere Energy | -10.07% |

Focused Opportunity Featured Company:

Comcast (CMCSA)

Comcast is the largest U.S. cable system operator with more than 30 million customer relationships. Comcast also owns NBC Universal, theme parks and SKY, a Pan-European Satellite TV broadcaster. It’s been about a year since the bidding war between Comcast and Disney for the Fox and SKY assets and Comcast’s business results continue to improve, notwithstanding the slow melting ice cube of the cable TV bundle. The broadband internet business continues to promote healthy subscription growth as it fills the cord-cutting streamers’ appetite. Comcast currently trades at a multiple of 8-9 times operating income and is well positioned to continue to grow and prosper as a true diversified media content and distribution juggernaut.

Equity Income Portfolio

Equity Income Portfolio Commentary and Thoughts

Our Equity Income Portfolio, like our other three, is a concentrated portfolio. Equity Income consists of high-quality companies with sustainable competitive advantages with average to above average dividend yields, along with the potential for dividend growth. The portfolio’s objective is to offer the opportunity for attractive total returns with the possibility of slightly higher income.

Equity Income, like Select, Focused Opportunity and International, is a go anywhere portfolio that is style and capitalization agnostic.

In the third quarter, the Equity Income Portfolio returned 5.02% (gross) and is up 17.59% YTD (gross).

Ten Largest Investments

September 30, 2019

| Year Acquired | Year Acquired | ||

|---|---|---|---|

| JP Morgan | 2007 | Home Depot | 2004 |

| Walmart | 1998 | Bristol Myers Squibb | 2018 |

| Exxon | 1998 | Intel | 2019 |

| Chevron | 2017 | Target | 2018 |

| Cisco Systems | 1998 | Pepsi | 2009 |

Portfolio Activity: During the third quarter, we made no portfolio changes.

Performance Attribution

| Contributors | Detractors | ||

|---|---|---|---|

| Newell Brands | +23.00% | Invesco Ltd. | -17.53% |

| Target | +22.97% | Cisco Systems | -9.74% |

| UPS | +16.36% | Exxon | -7.77% |

| Home Depot | +10.34% | Cummins Inc. | -5.89% |

| Bristol Myers Squibb | +9.81% | Chevron | -5.00% |

Equity Income Portfolio Featured Company:

Newell Brands

Newell is an American worldwide marketer of consumer and commercial products such as Rubbermaid, Coleman, Paper Mate, Elmer’s, Graco, Calphalon, Mr. Coffee and Yankee Candle just to name a few. Newell’s debt-fueled acquisition of many of these brands over the years has not panned out as successfully as management hoped. The sentiment around the company seems to be changing as more aggressive cost cutting and non-core asset sales seem to be starting to move the needle in optimizing the portfolio of companies. By focusing on the brands with the most attractive margins and growth potential, Newell can drive operational efficiency while improving financial flexibility and free cash-flow productivity. Newell is tremendously underearning its potential and could offer quite a bit of upside with the shares around $16.00.

International Portfolio

International Portfolio Commentary and Thoughts

Our International portfolio is also highly concentrated in what we feel are superior, growing businesses. The portfolio’s objection is to expose us as long-term investors to other opportunities worldwide. The mandate allows for unlimited geographical reach and can own any size capitalization business. Most of the world’s growth is outside the U.S. and therefore, we hope to capitalize on that by owning great businesses at fair prices.

Ten Largest Investments

September 30, 2019

| Year Acquired | Year Acquired | ||

|---|---|---|---|

| Nestle | 2002 | Safran | 2018 |

| Alibaba | 2018 | JD.Com | 2018 |

| New Oriental Education | 2018 | Ten Cent Holdings | 2018 |

| Fiat Chrysler | 2018 | Development Bank of Singapore | 2018 |

| Ferguson | 2019 | Airbus Group | 2018 |

Portfolio Activity: During the third quarter, we made no portfolio changes.

Performance Attribution

| Contributors | Detractors | ||

|---|---|---|---|

| New Oriental Education | +12.54% | Teva Pharmaceutical | -26.18% |

| Safran | +7.57% | Baidu.com | -12.92% |

| Sanofi | +6.33% | Siemens AG | -10.68% |

| Nestle | +6.13% | Encana | -10.51% |

| Ferguson | +2.26% | Ten Cent Holdings | -10.43% |

International Portfolio Featured Company:

New Oriental Education

Formed in 1993, New Oriental is the largest and most recognized provider of private educational services in China. The company has over a 38.1 million student enrollment. The company has a network of 1,100 learning centers, schools and bookstores. The mission of New Oriental is primarily to provide after-school tutoring and entrance exam prep as well as private schooling. China has tremendous barriers to college entry with roughly only 1 in 50 students qualifying. The college entrance exam process is extremely difficult without the testing prep classes New Oriental provides. Occupancy is growing by 20% per year, driving 30%+ increases in revenue and profit for New Oriental. The stock is not cheap, but the runway for growth appears very attractive.

Appendix 1

Live Oak Private Wealth Investment Philosophy

Three Pillars

We consider potential losses before gains. We think about multiple scenarios that could affect us. We ask how much we might lose before we ask how much we might make.

We focus on absolute returns, not relative returns. Our goal is to lose less than the market. We don’t manage to a benchmark.

We do not focus on the macroeconomic environment. We focus on truly great businesses we can invest in at a fair price.

Our Beliefs

We believe your lifetime investment results will be mostly governed by two variables: behavior and asset allocation.

We consider the three quotes below by two very famous investors daily in our thoughts, research and work.

“To buy when others are despondently selling and to sell when others are avidly buying, requires the greatest

fortitude and pays the greatest reward.”

John Templeton

“Be fearful when others are greedy and greedy when others are fearful.”

Warren Buffett

“Price is what you pay, value is what you get.”

Warren Buffett

Guiding Principles

- A share of stock represents a share in the ownership of a business.

- A stock exchange is nothing more than an auction place that provides a convenient means for exchanging your ownership in a business for cash and vice-versa.

- Our investment approach would be akin to applying a private equity mindset to investing in public markets.

- We limit our search for qualifying investments to good businesses. They have identifiable, sustainable competitive advantages.

- Risks to us is permanently losing capital over a five-year time horizon. Market volatility is not risk to us.